For all the uncertainty and concerns the US-Iran-Israel war is causing for oil prices, interest rates, inflation, the global economy and equity prices, it seems US analysts are not concerned. In fact, the earnings picture for corporate America remains, perhaps surprisingly, intact — even improving.

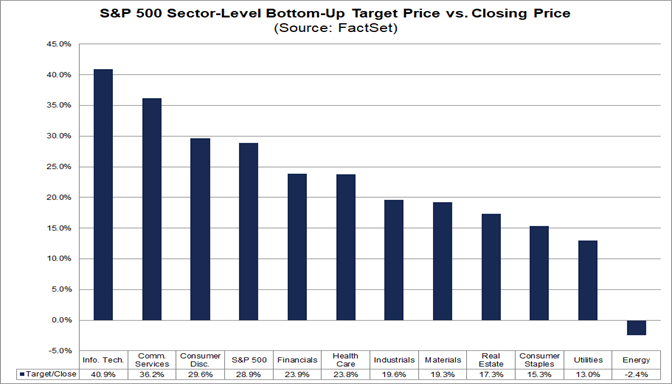

Over the past three months, analysts have raised their projected earnings for the S&P 500 companies by 8%. Factset’s data as of March 26 shows the S&P 500 bottom-up analyst price target implies 28.9% upside with 8 of 11 sectors showing analysts raising price targets.

The damage to sentiment, however, is real and visible. As of yesterday’s close the tech-heavy Nasdaq has slipped firmly into correction territory, down more than 10% from its October peak. The Dow Jones and the S&P 500 are both flirting with the same threshold, teetering on the edge of a correction of their own. For investors who had grown accustomed to a relentless grind higher through much of 2024 and into early 2025, the pullback has been jarring.

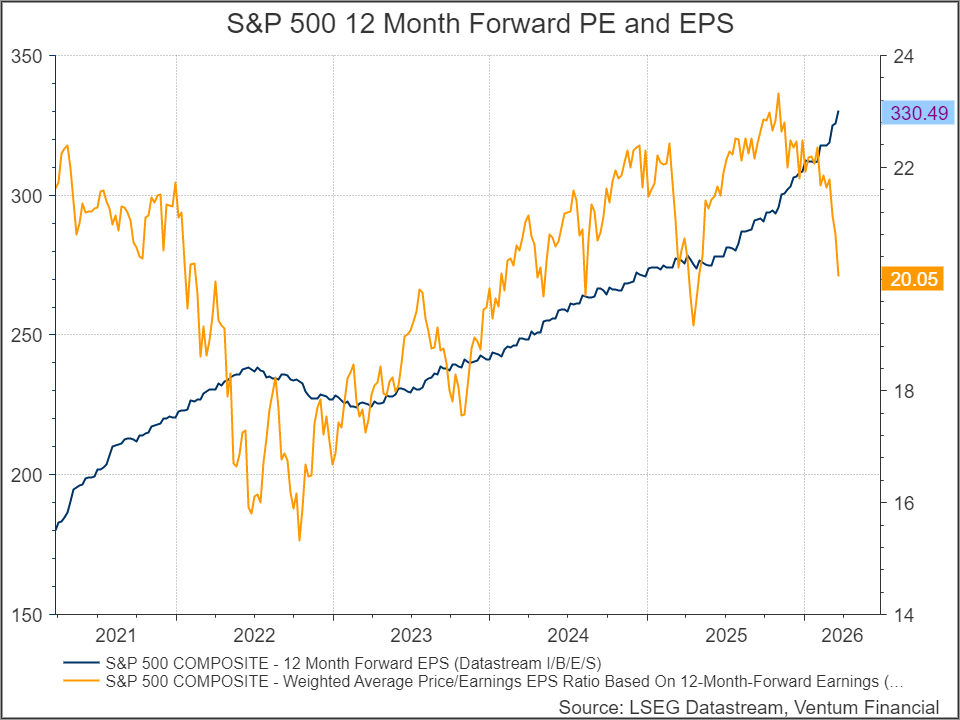

But it is worth being precise about what is actually falling here. This is, at its core, a decline in investor sentiment — a compression of the premium that markets were willing to pay for future earnings — rather than a deterioration in the earnings estimates themselves. The S&P 500’s forward price-to-earnings multiple has retreated from its peak of over 23 times to just around 20 times. That is a meaningful re-rating, and it explains much of the index-level pain. Investors are paying less for each dollar of future profit, not because those profits are disappearing, but because uncertainty has a price.

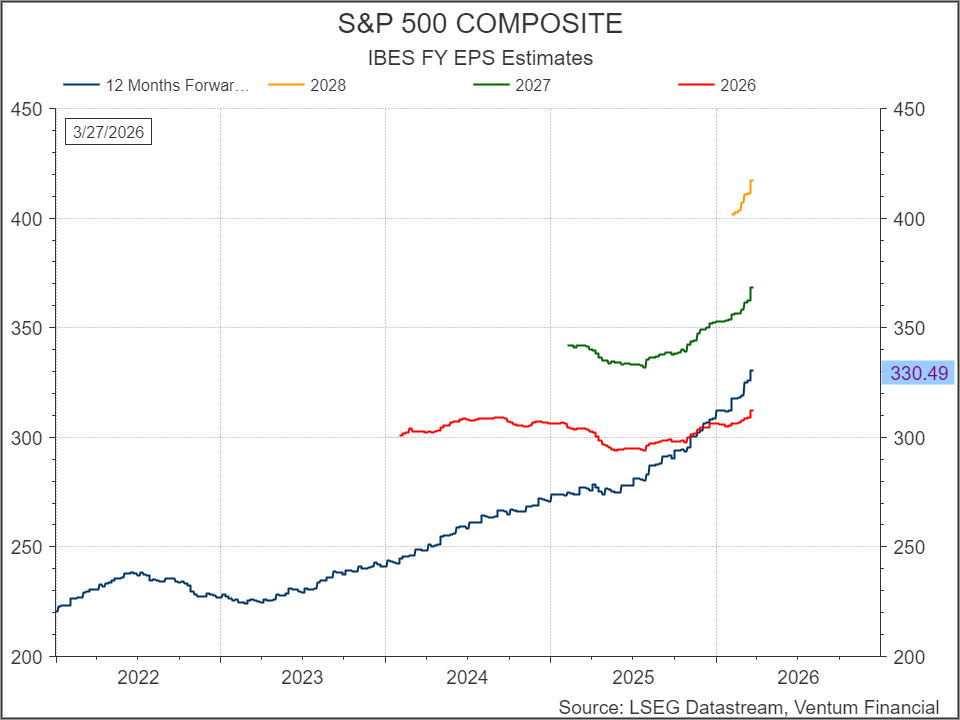

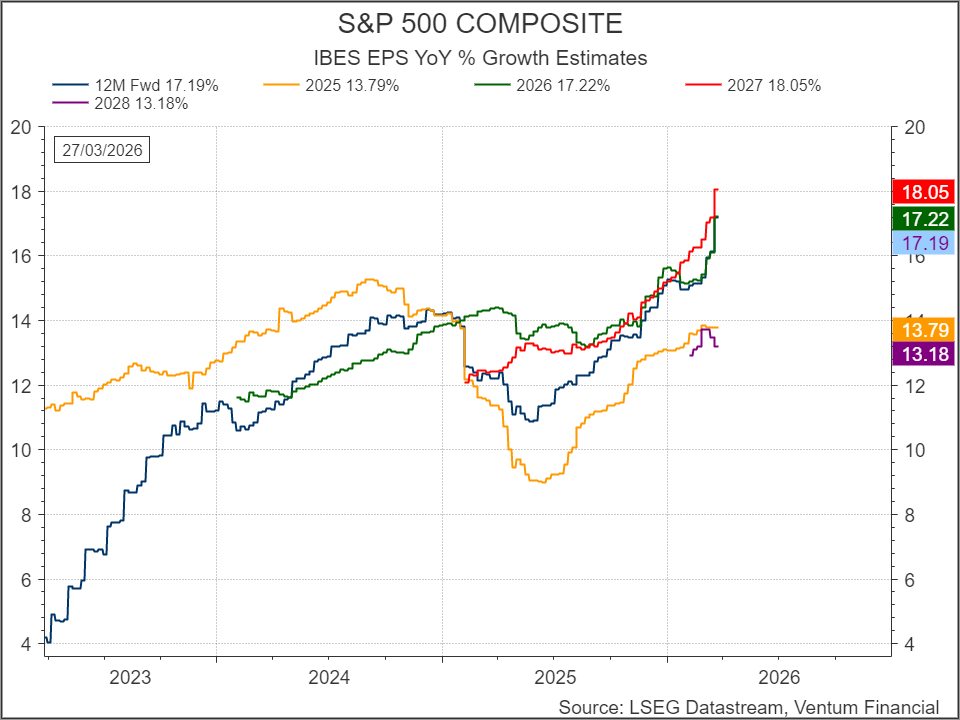

And the profits, for now, are holding up remarkably well. The twelve-month forward EPS level sits at $330.49 — a figure that has risen steadily and with remarkable consistency since 2022, barely flinching in the face of the current turbulence. Full-year estimates for 2026 sit near $311, with 2027 already pencilled in above $365 and 2028 approaching $415.

The trajectory is not just high — it is accelerating. Twelve-month forward EPS growth is now running at over 17%, its strongest pace since 2020.

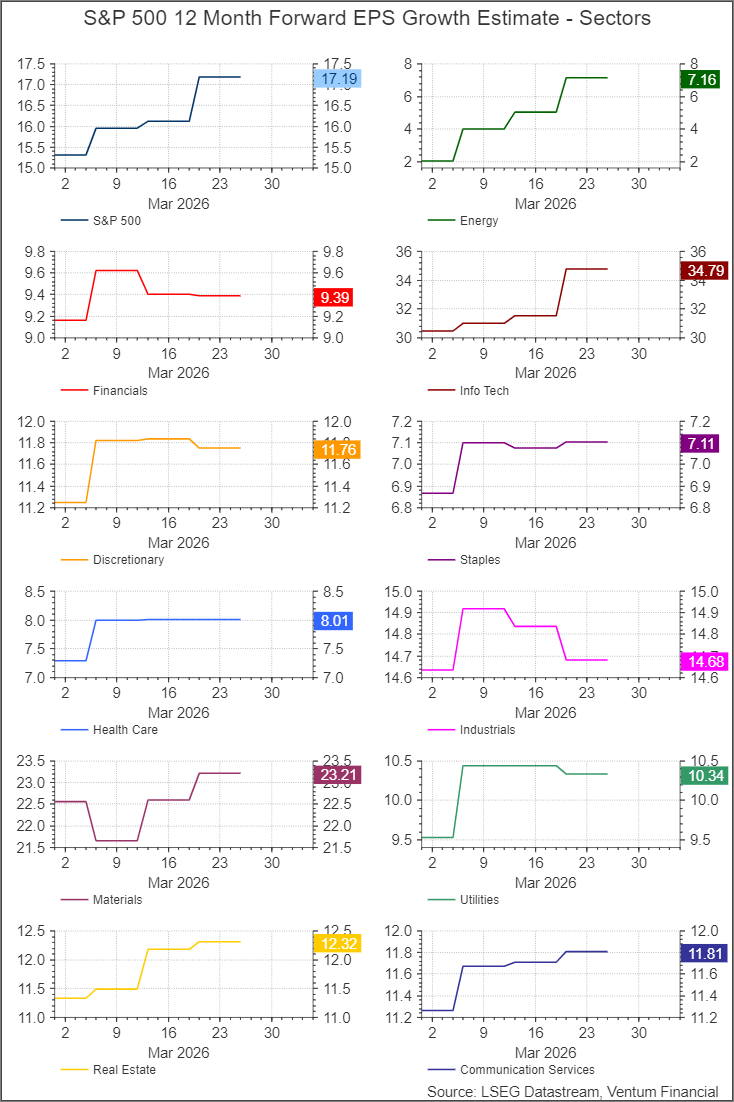

The sector-level picture is where things get genuinely interesting. Energy has seen the most dramatic upward revision this month, with its 12-month forward EPS growth estimate surging from around 2% at the start of March to above 7% by month’s end. That is the kind of move that reflects a rapid repricing of the commodity and geopolitical environment — energy, unsurprisingly, benefits from the sky high price of crude oil.

What is more striking, though, is the breadth of the revision cycle. All eleven S&P 500 sectors have registered positive earnings revisions over the course of this month. Every single one. Even Industrials — a sector burdened by capital intensity and interest rates — has come in flat to modestly higher.

The tension, then, is clear — and it cannot hold indefinitely. Markets are pricing in more fear. Earnings estimates are pricing in more growth. These two realities are pulling in opposite directions, and the rope between them is fraying. Something will have to give.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 – 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre – Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.