Over the weekend, escalation in hostilities between the U.S., Israel and Iran sent a clear risk-off signal through financial markets. On Monday at the open, all three major U.S. indices were lower — the S&P 500 off roughly 1% and the tech-heavy Nasdaq down about 1.5% — as traders repriced risk assets in the face of heightened geopolitical uncertainty. Commodities quickly reflected the potential for disrupted Middle East supply, with WTI crude oil rising above $70 a barrel and safe-havens like gold and the USD rallying sharply as traders sought protection.

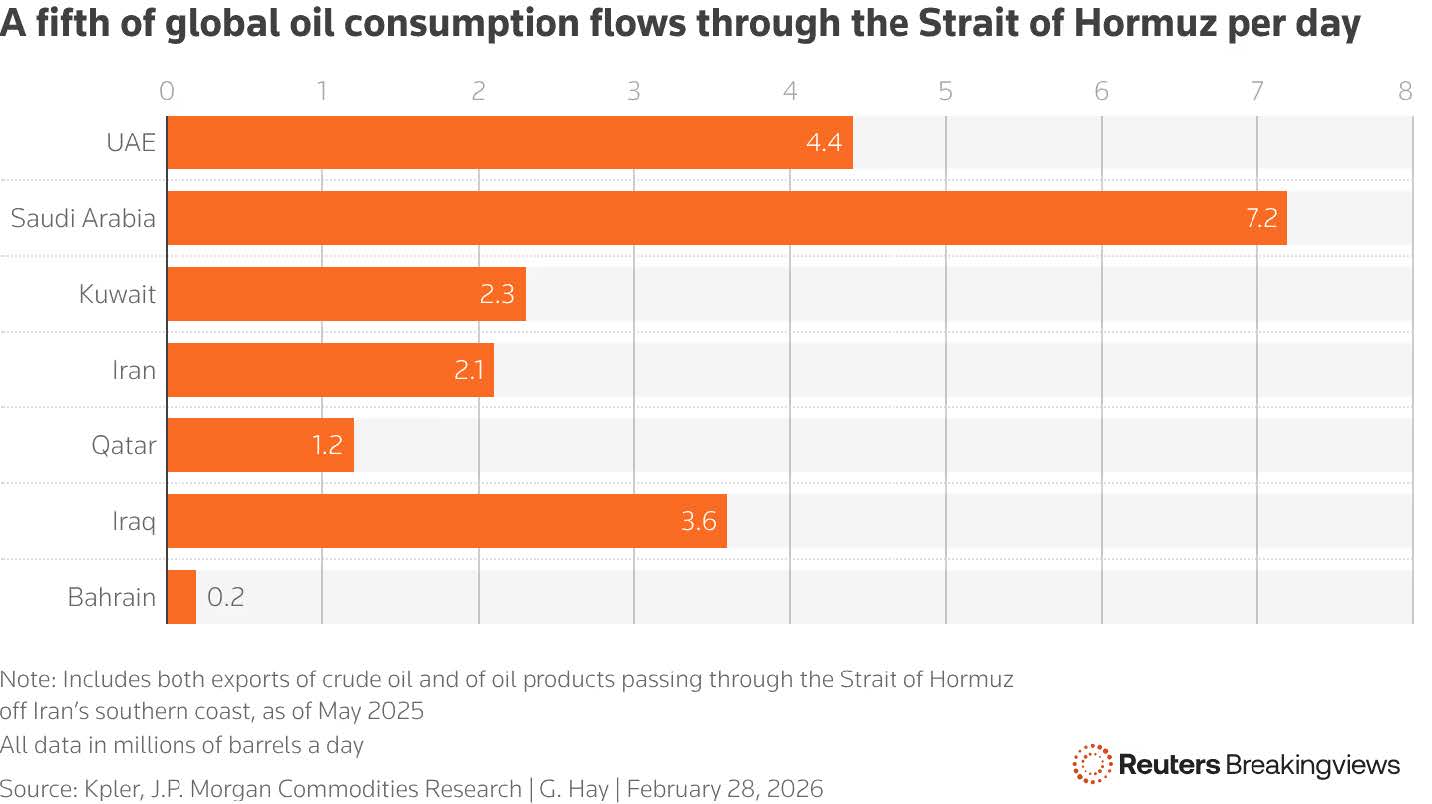

The oil market reaction was grounded in the strategic importance of the Strait of Hormuz. Roughly one-fifth of global crude oil consumption transits this chokepoint each day, with major producers including Saudi Arabia (≈7.2 mmb/d), the UAE (≈4.4 mmb/d), Iraq (≈3.6 mmb/d) and Kuwait (≈2.3 mmb/d) relying on uninterrupted flows.

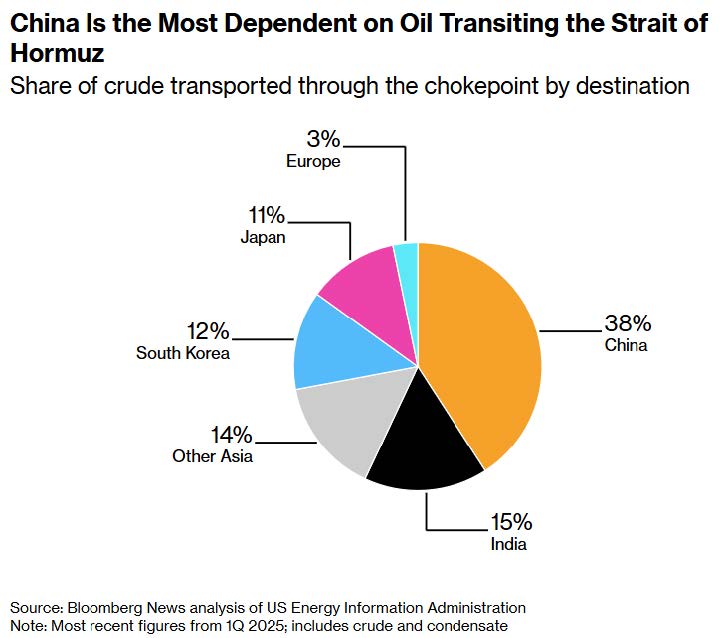

According to Bloomberg, a significant share of that crude ultimately fuels East Asian demand — notably China (≈38%), India (≈15%), South Korea (≈12%) and Japan (≈11%) — underscoring how disruptions can reverberate through global energy balances.

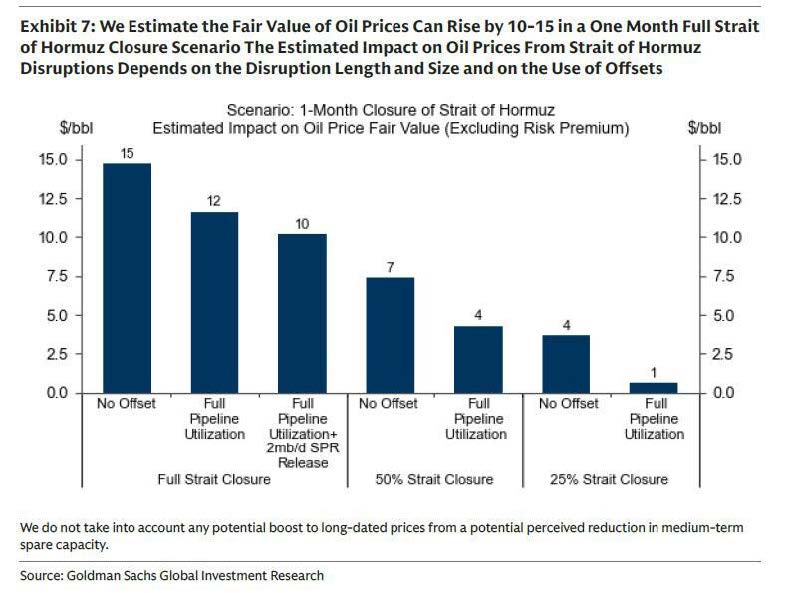

Market participants are also sensitive to the duration and magnitude of potential disruptions. Research from Goldman Sachs over the weekend on the impact of a full one-month closure of the Strait of Hormuz suggests fair-value oil prices could rise $10–$15/bbl or more absent offsets from strategic reserves or alternative supply routes. Even a partial closure (25–50%) could lift values by several dollars per barrel, depending on available pipeline capacity and storage releases — a reminder of the leverage that supply chokepoints carry in an already tight market.

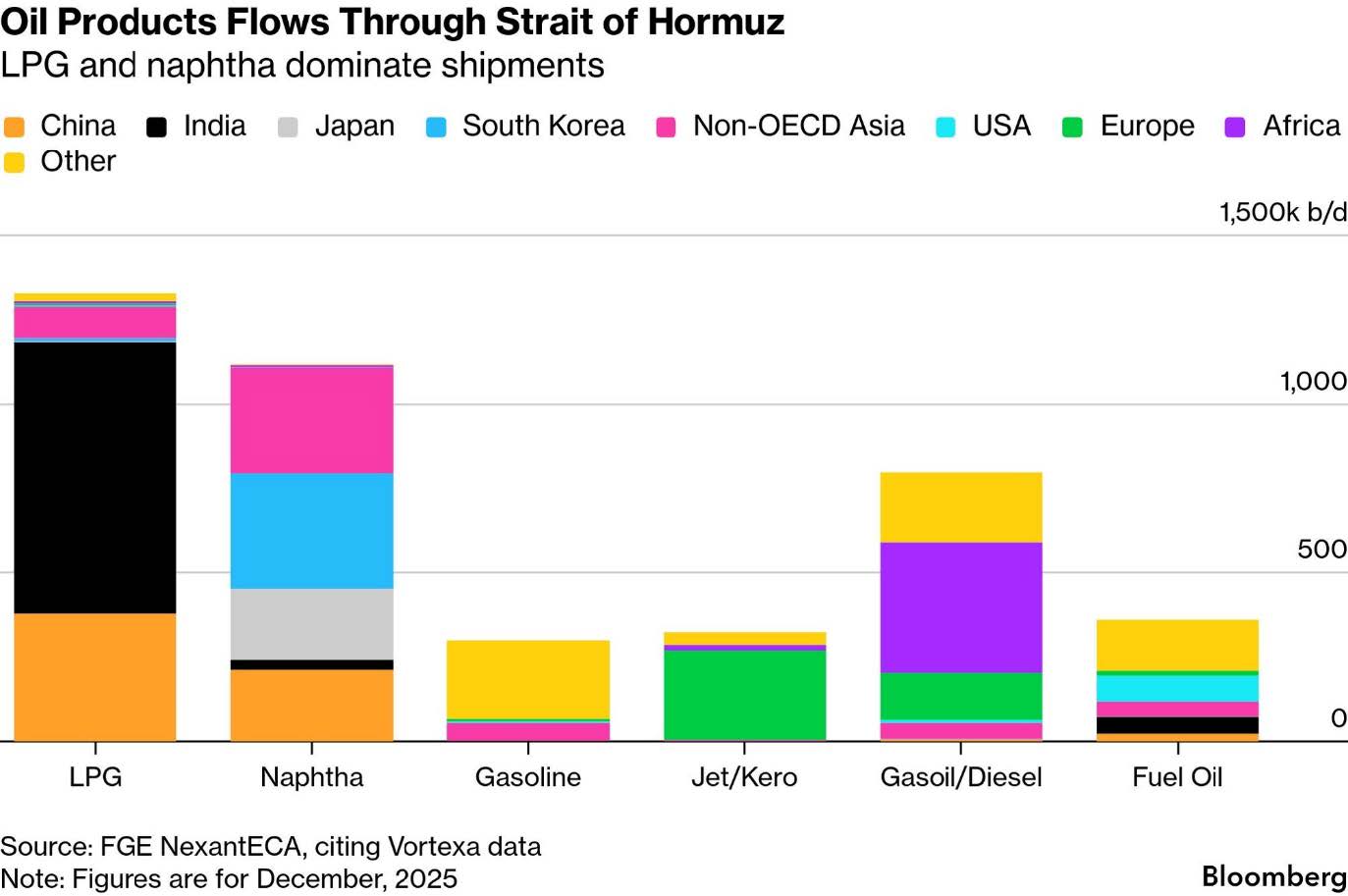

Importantly, the vulnerability of the Strait of Hormuz extends well beyond crude oil. Refined products flowing through the chokepoint are heavily concentrated in LPG and naphtha, key feedstocks for petrochemicals and plastics production. Asia is the dominant destination across these product categories, meaning any disruption would ripple directly into industrial supply chains, manufacturing inputs, and consumer goods pricing — not just transportation fuels.

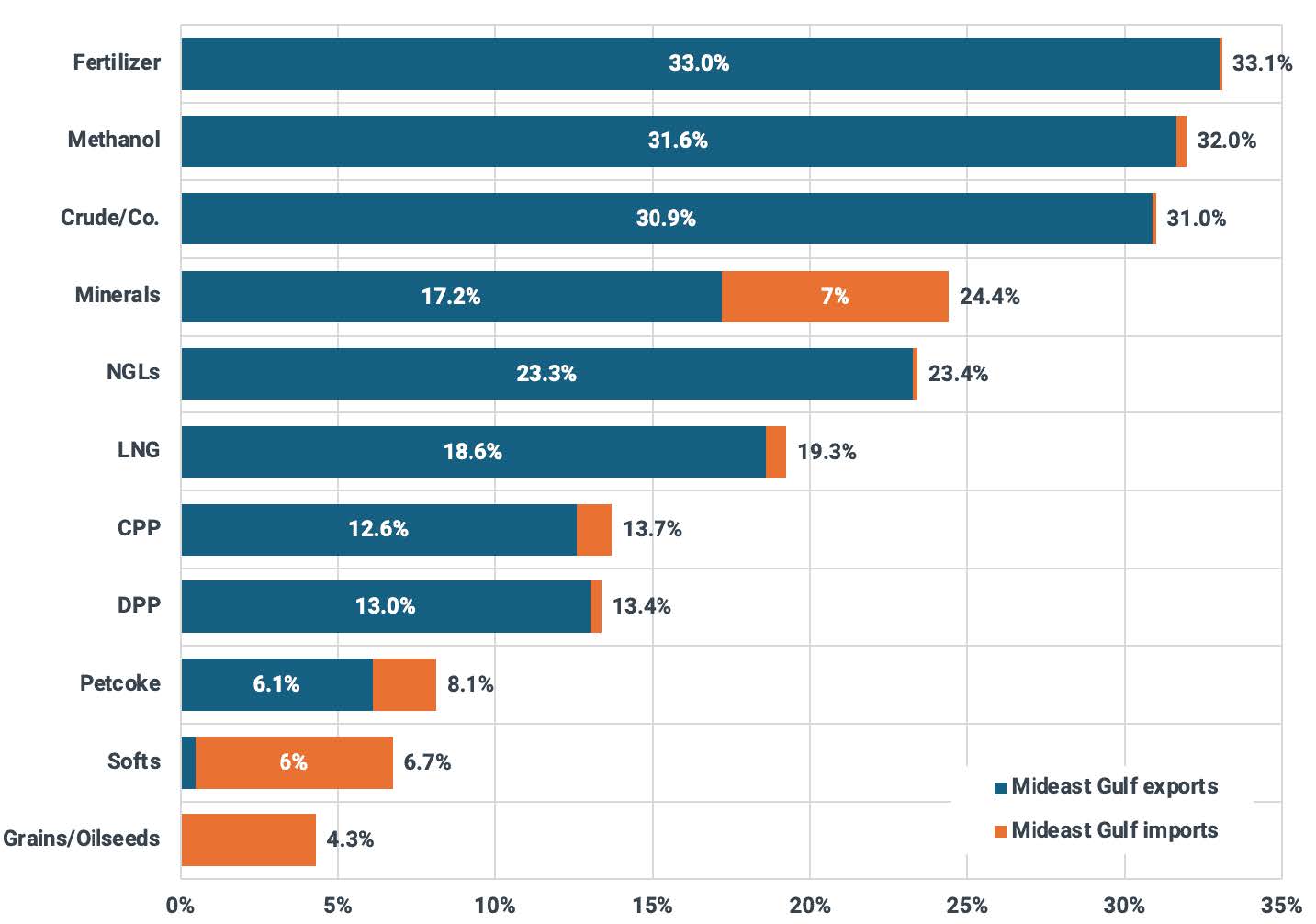

Moreover, the Middle East Gulf plays a critical role in global petrochemical and fertilizer trade. Roughly one-third of global exports of fertilizers, methanol, and crude oil products originate from the region, alongside meaningful shares of LNG and natural gas liquids. This underscores that a disruption would not only pressure crude benchmarks like WTI and Brent, but could also tighten markets for agricultural inputs, industrial chemicals, and energy-intensive materials — broadening the inflationary channel beyond gasoline into food production and core goods.

Source: KPLER

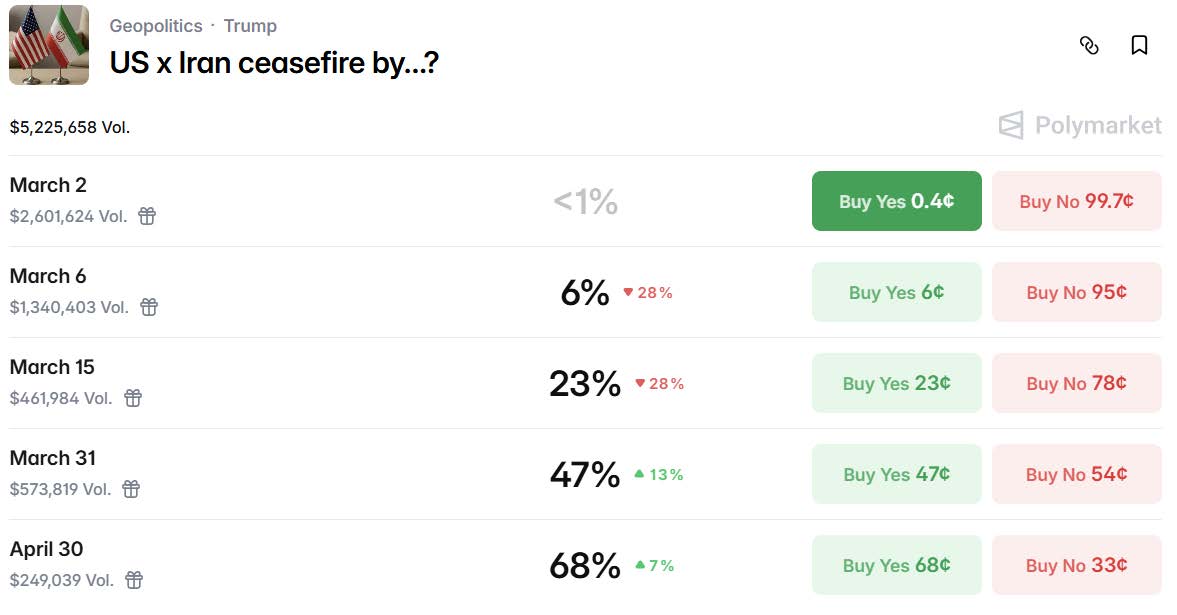

On the broader geopolitics front, market-based probability indicators show increasing expectations of a negotiated ceasefire later this month or into April, with a rapid shift from sub-1% odds earlier in March toward a majority probability of de-escalation by late April.

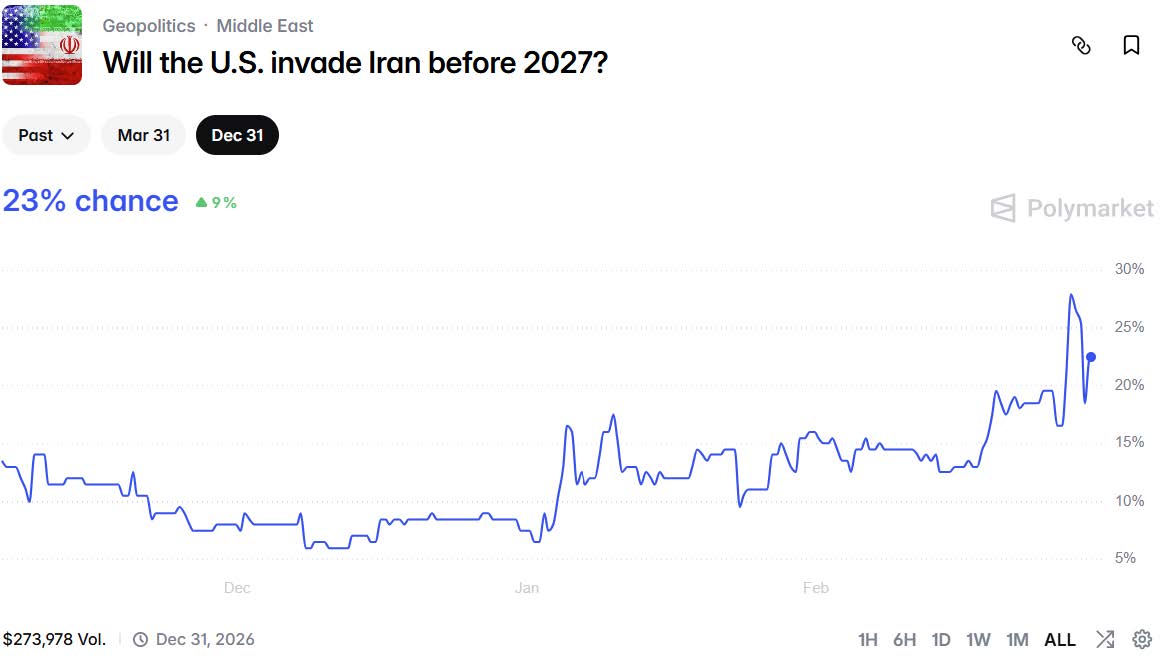

Similarly, longer-dated contracts still imply only modest chances of a full-scale invasion of Iran before 2027.

Taken together, the price action reflects a sharp but contained repricing of risk, concentrated in energy and safe-haven assets rather than a wholesale sell-off across global markets. This suggests investors see heightened short-term volatility rather than an extended disruption to supply or to economic growth.

As of now, the market is not pricing in a prolonged conflict between the U.S., Israel and Iran and should have limited effects in terms of macroeconomic instability. Transmission of higher energy prices into sustained inflation appears muted — 1-year breakeven inflation currently sits at ~2.89%, well below the multi-year peak above 4% seen on Feb. 4 — indicating that markets continue to expect inflation pressures to moderate absent a deeper or lengthier supply shock.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 – 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre – Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.