Canadian and US Economy: The U.S. economy is slowing but resilient, with business investment — particularly AI capex offsetting weakness in other sectors. In Canada, economic growth is expected to be weaker in 2026,while wage growth is running higher. The Middle East conflict has pushed up oil, fertilizers, aluminum and other inputs, and is raising the worry of stagflation – slowing growth meets rising inflation.

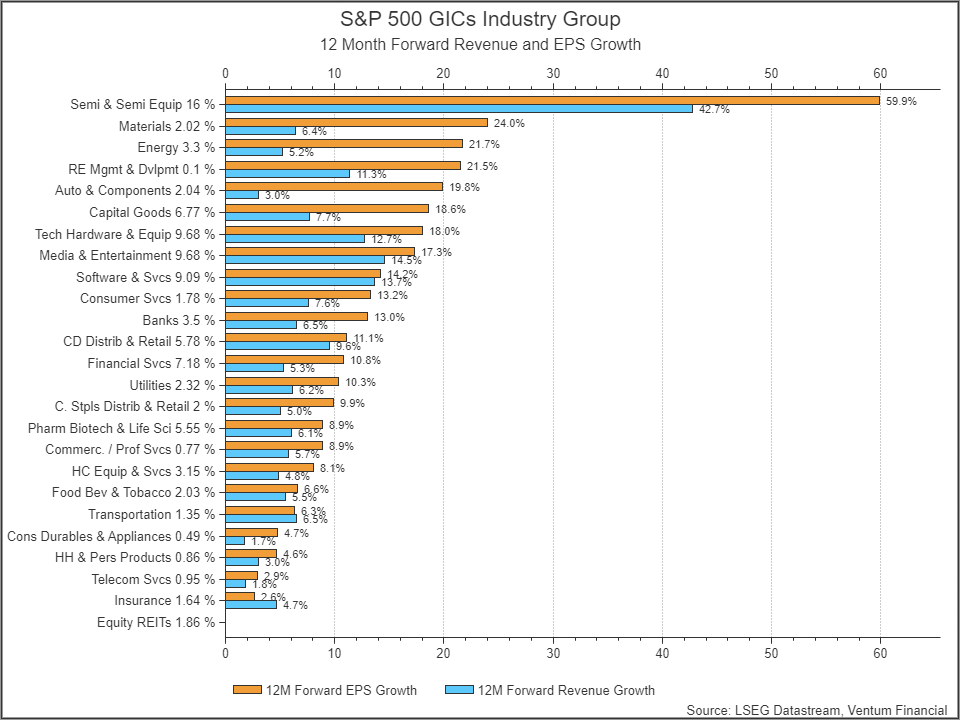

Equity Markets: After a difficult March, equity markets rebounded strongly in April on ceasefire optimism and robust AI-related earnings, with North American indices posting gains of 3–12% month to date. While the velocity of the reversal underscores the ongoing volatility, the rally appears fundamentally grounded, with analysts forecasting positive revenue and earnings growth across all major S&P 500 industry groups over the next 12 months. Technology stocks account for most of the S&P 500 performance since the start of the Middle East war. Semiconductors and semiconductor equipment companies remain a key highlight, with 12-month forward earnings-per-share growth projected at roughly 60% and revenue growth expected to exceed 40%, reinforcing the sector’s central role in the AI-driven investment narrative.

Bond Market: U.S. and Canadian yields have pulled back from their March peaks on ceasefire optimism, but remain elevated relative to late 2025, suggesting markets aren’t yet convinced the inflation threat has passed. With oil prices bouncing back and stick inflation, the Bank of Canada and US Fed are facing a tricky situation with little room to cut rates.

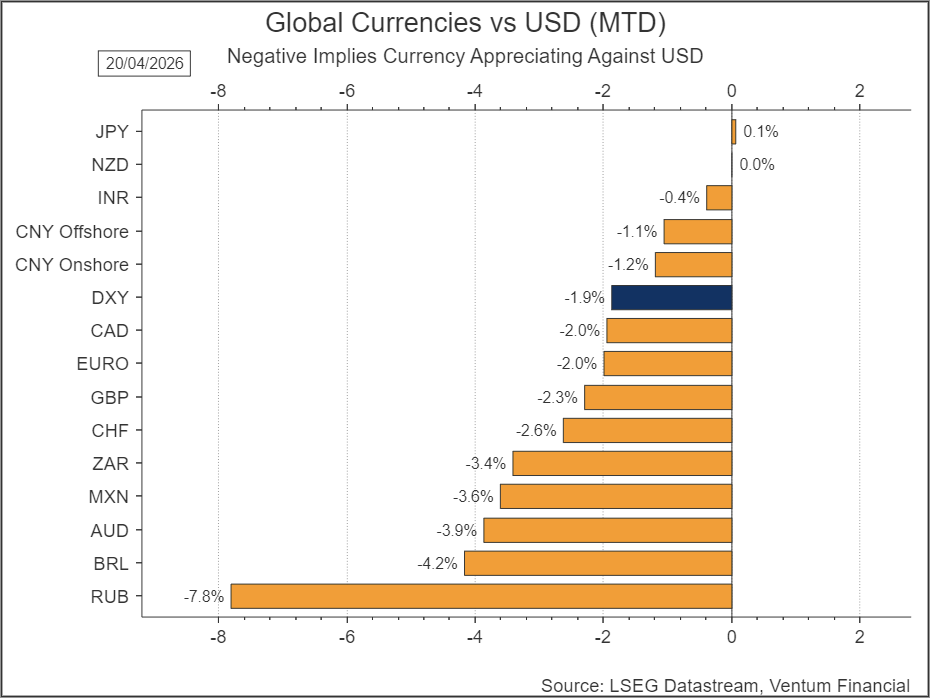

Commodities and Currencies: While oil prices started the month sharply lower, at time of writing, the lack of an Iran/US truce has reversed most of its decline. The path to peace remains elusive, and, until a ceasefire agreement is obtained, energy prices and markets will remain volatile. Gold and silver rallied early in April on ceasefire optimism before giving back gains as prospects faded, leaving both metals flat on the month at the time of writing. The USD has weakened against every major currency except the yen as its safe-haven appeal faded.

Portfolio Strategy: We expect markets to remain highly volatile and headline driven, significantly by the US-Iran conflict and the AI technology sector. Technology continues to be the key market driver. Given the resilient jobs market and consumer, and the positive outlook for corporate revenue and earnings, we stay positive on equity prices with bias to the technology, industrial, materials, consumer services and financial sectors.

Equity Markets

April marked a dramatic reversal from March’s risk-off environment. After the Strait of Hormuz disruption sent Brent crude to nearly $120/bbl and triggered broad equity declines in March, April’s narrative pivoted sharply as ceasefire signals emerged between the U.S., Israel, and Iran. A two-week ceasefire announced in early April — with Iran committing to allow safe passage of ships through the Strait — sent energy prices plunging and unleashed a powerful relief rally across global equity markets.

The S&P 500 closed above the 7,000 level for the first time in history on April 15, setting a record high. The Nasdaq Composite logged its longest consecutive winning streak since 2009, driven by a re-engagement with technology and AI-linked names. However, the recovery has not been without volatility — renewed U.S.-Iran tensions over the weekend of April 19-20 briefly interrupted the rally, a reminder that the geopolitical situation remains fluid.

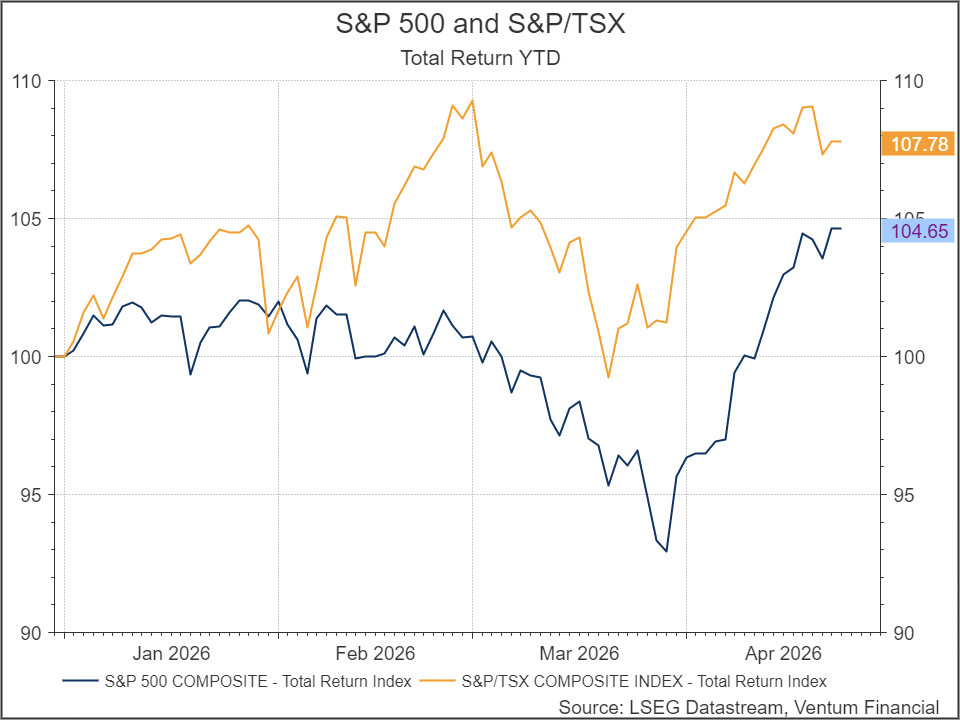

Energy sold off for most of the month, the US dollar weakened, and rate-sensitive sectors roared back. April rewarded those who stayed invested, but the speed of the reversal is a reminder of how volatile this market is and how quickly geopolitical sentiment can reprice entire asset classes. Month to date of this report, the technology heavy Nasdaq Index, not surprisingly, is leading North American indices with gains close to 12%, followed by the S&P 500 +8%, Dow + 5% and S&P/TSX Composite of +3%.

Technology company earnings, especially AI related, took centre stage, with quarterly results justifying investor enthusiasm: The ceasefire provided the spark, but with semiconductor sector profits tracking nearly +60% in 12-month forward EPS growth, and over 42% revenue growth, this rally has real earnings behind it albeit concentrated. Moreover, analysts are forecasting that all the major S&P 500 industry groups will post positive revenue and earnings growth in next 12 months. On the TSX, analysts are expecting the Financial Services, Materials and Hardware Equipment industry groups to show the fastest earnings growth.

US Economy

The latest U.S. data presents a nuanced picture: growth is showing early signs of deceleration, yet the consumer continues to hold up better than the headline numbers suggest. The Atlanta Fed’s GDPNow model has revised its Q1 2026 estimate down sharply to +1.24% — a significant step down from the above-trend readings that characterized much of 2024 and early 2025. Digging into the components, the drag is concentrated in net exports (-0.87%) and private residential investment (-0.31%), as uncertainties about growth, the war in the Middle East, and high interest rates continue to weigh. Crucially, consumer spending remains a positive contributor at +0.95%, even as it slowed from over 2% at the beginning of the year, and non-residential investment increased to +0.90%, up from less than 0.30% at the start of the year — suggesting that CapEx in AI will drive growth this quarter as consumers pulled back.

The labour market tells a similarly mixed but resilient story. Non-farm payrolls for March came in at 178,000 total, with private payrolls contributing 186,000 — a solid print that comfortably offsets the government sector drag of -8,000. The unemployment rate ticked up slightly to 4.3%, near the top of its recent range but still historically low. Average hourly earnings growth has moderated to 3.5% year-over-year, consistent with a labour market that is cooling gradually rather than cracking. Importantly, there are no signs of broad-based layoffs; the softening reflects a slower pace of hiring rather than deteriorating conditions. On the consumption side, March retail sales delivered a strong +1.70% month-over-month beat, with the year-over-year pace accelerating to +3.97%. Even stripping out volatile categories, the underlying trend remains firm: retail ex-motor vehicles and parts rose +1.90%, and the core control group posted +0.70%.

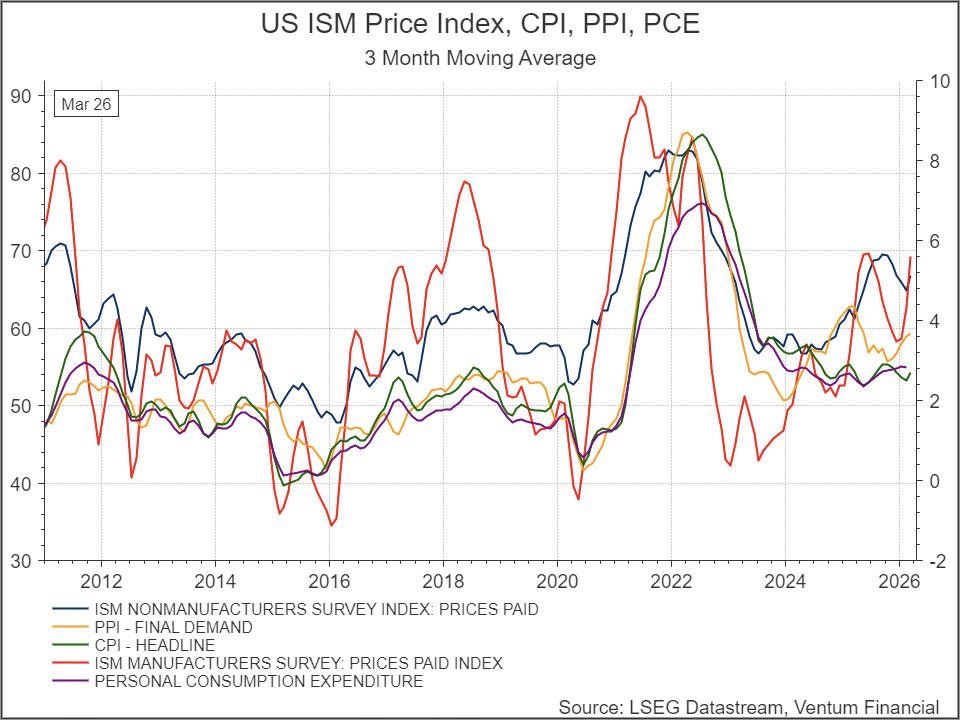

Headline and core CPI increased in March to 3.3% and 2.6% respectively, reflecting higher energy prices stemming from the war in the Middle East — a reminder that the inflation story is not yet resolved, and that the Fed’s path back to easing remains contingent on geopolitical developments.

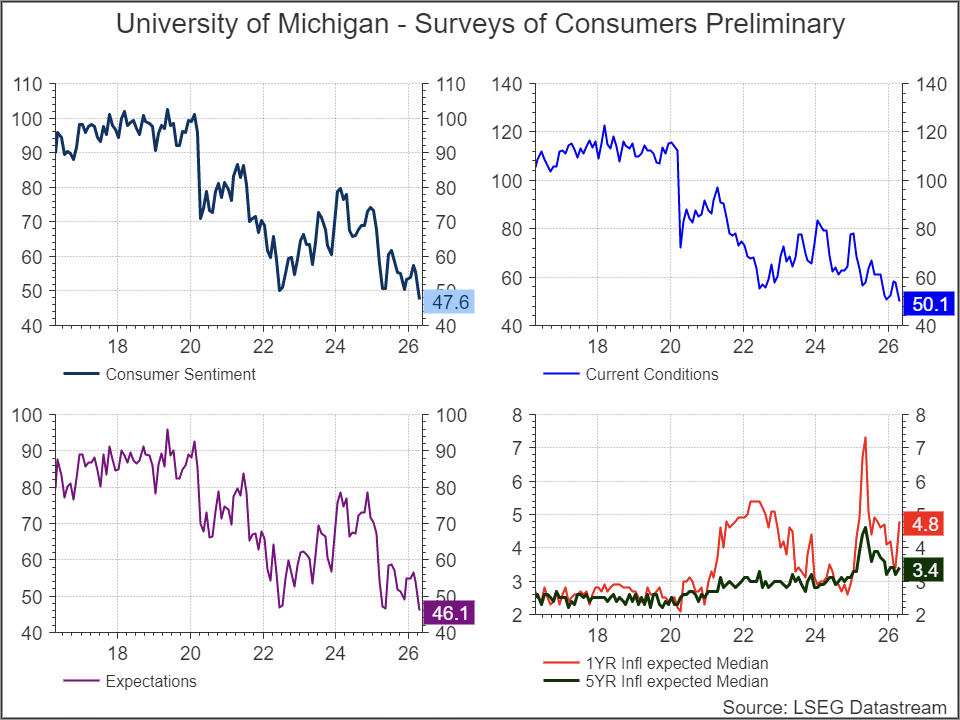

A key risk to the constructive narrative is the consumer and business confidence backdrop. The University of Michigan Consumer Sentiment index has fallen to 47.6 — an all-time low, surpassing even the lows of May 1980 — with current conditions at 50.1 and expectations at 46.1. One-year inflation expectations have spiked to 4.8% and five-year expectations sit at 3.4%, both well above the Fed’s target. We believe current consumption is being sustained primarily by higher-income households and elevated household wealth — but this is a narrow foundation. Should equity markets correct, credit conditions tighten further, or energy prices re-accelerate, the pullback in spending could broaden quickly — and with business confidence similarly fragile, the feedback loop between sentiment and activity bears close watching in the months ahead.

The U.S. growth story is shifting from acceleration to moderation—not contraction. The recent pullback in GDP forecast largely reflects trade-related volatility and a consumer that is recalibrating rather than retrenching. At the same time, the near-term growth baton is passing to business investment, particularly AI-driven capex. With the labour market holding steady and retail spending continuing to surprise to the upside, consumption should remain a meaningful pillar of growth through mid-2026. The key risk is that rising inflation and interest rates—potentially driven by higher energy prices—begin to constrain both consumers and businesses more materially.

Canadian Economy

Canada’s labour market is sending conflicting signals heading into April. The unemployment rate edged up to 6.7% in March — near the top of its two-year range — with job creation skewing toward part-time work (+15,200 part-time, -1,100 full-time), suggesting an economy treading water rather than gaining momentum.

The one countervailing force is wages. Average hourly earnings for permanent employees have reaccelerated sharply to 5.1% year-over-year — the strongest pace in recent memory — reflecting structural labour scarcity driven by demographics and tighter immigration policy rather than genuine demand strength. This creates an uncomfortable paradox for the Bank of Canada: the labour market is weakening, yet wage pressures limit how aggressively it can cut rates, particularly with energy-driven inflation risks still present.

On inflation, Canada’s March CPI headline came in at +2.4% year-over-year, with the month-over-month reading a more modest +0.9%. The dominant driver remains energy at +13.1% MoM — a direct transmission of the Middle East conflict into Canadian pump prices — while transportation (+3.7% YoY) and food (+4.0% YoY) continue to keep everyday costs elevated for households. Encouragingly, shelter inflation is decelerating at +1.7% YoY, reflecting the ongoing normalization of rents as population growth slows. Core inflation — all items excluding food and energy — held at +2.5% YoY, keeping the Bank of Canada in a difficult position: headline pressures are largely externally driven, but core is sticky enough to prevent aggressive easing. The market is pricing in 65% chance for hike by October.

Canada’s labour market is weaker than the headline suggests, and inflation is being kept alive by energy rather than demand. The Bank of Canada is effectively caught — cutting risks re-igniting price pressures, while hiking weighs on an already fragile jobs market and consumer. Our view is that until the Middle East situation resolves and energy prices normalize, expect the Bank to remain on hold and the Canadian outlook to stay cautious.

Sector Performance – Tech continues to lead

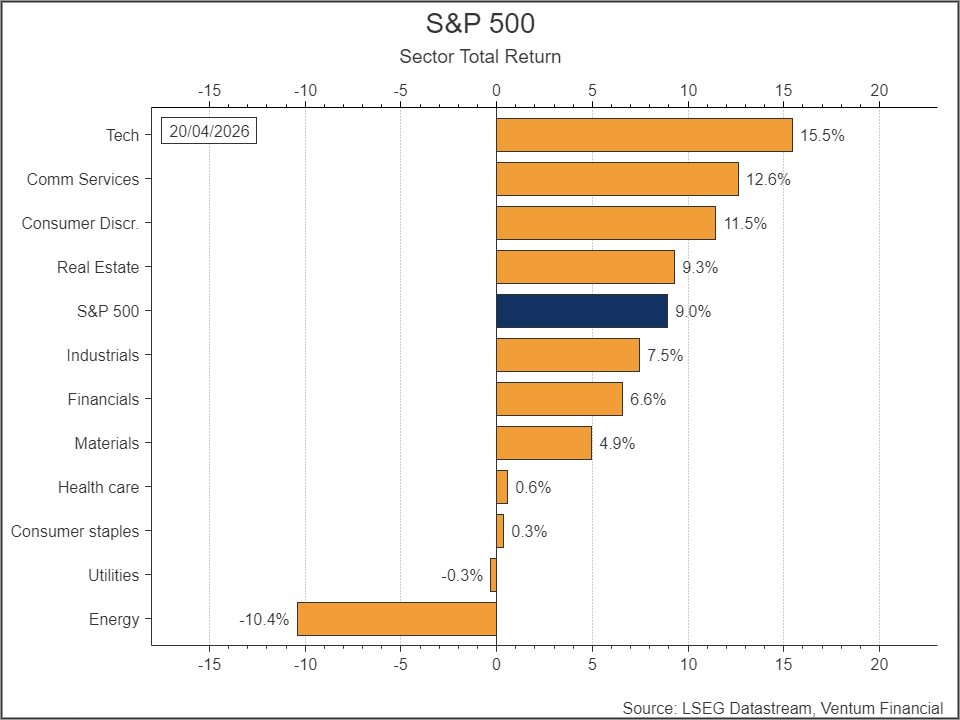

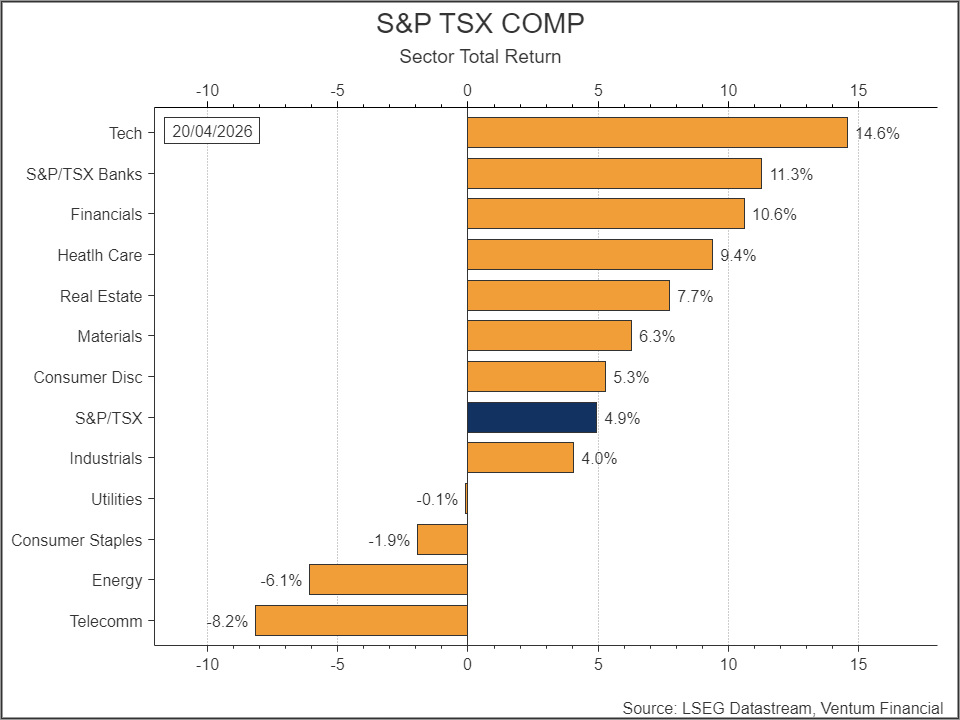

April’s sector returns through the 20th tell a clear and consistent story on both sides of the border: the ceasefire-driven reversal of March’s energy shock unleashed a powerful rotation back into growth and rate-sensitive sectors, while energy — March’s standout winner — became April’s biggest loser.

S&P 500 delivered a +9.0% total return month-to-date, with Technology leading at +15.5%, followed by Communication Services at +12.6% and Consumer Discretionary at +11.5% — all three sectors directly benefiting from falling bond yields, easing inflation fears, and strong AI-driven earnings. On the downside, Energy gave back -10.4% as Brent crude retreated sharply on ceasefire news, and Utilities slipped -0.3% as the safe-haven bid that had supported defensives in March evaporated.

The S&P/TSX told a similar story, returning +4.9% overall return — a solid month to date, though trailing the tech heavy U.S., as Canada’s heavier energy weighting acted as a drag. Technology again led with +14.6%, with Banks and Financials close behind at +11.3% and +10.6% respectively as lower rate expectations supported valuations across the financial sector. Energy declined -6.1% and Telecom fell -8.2%, the latter reflecting ongoing structural pressures from competition and regulatory headwinds that are independent of the macro backdrop.

Bond Market

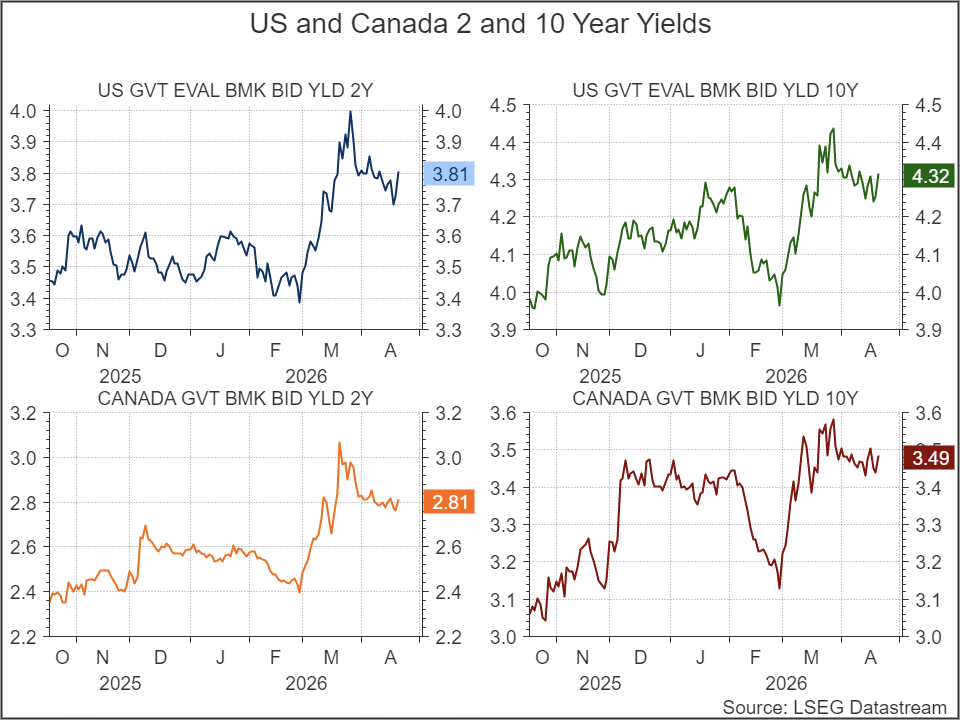

The U.S. 2-year and 10-year Treasury yields currently sit at 3.81% and 4.32% respectively, having pulled back from their March peaks as ceasefire optimism eased inflation fears — but remaining elevated relative to late 2025 levels, reflecting a market that is not yet convinced the inflation threat has passed. Canadian yields tell a similar story, with the 2-year at 2.81% and the 10-year at 3.49%, both having risen sharply since the start of 2026 and leaving the Bank of Canada with limited room to ease without risking a further currency and inflation impulse. The current situation leaves little room for the Bank of Canada and US Fed to cut rates anytime soon.

Commodities and Currencies

The U.S. dollar — which had benefited from safe-haven flows in March — weakened broadly, with the DXY down -1.9% month-to-date. Nearly every major currency appreciated against the USD: the CAD and EUR both gained 2.0%, GBP 2.3%, and commodity-linked currencies like AUD and BRL also rallied meaningfully — a sign that global investors are rotating back into risk as the geopolitical temperature cools.

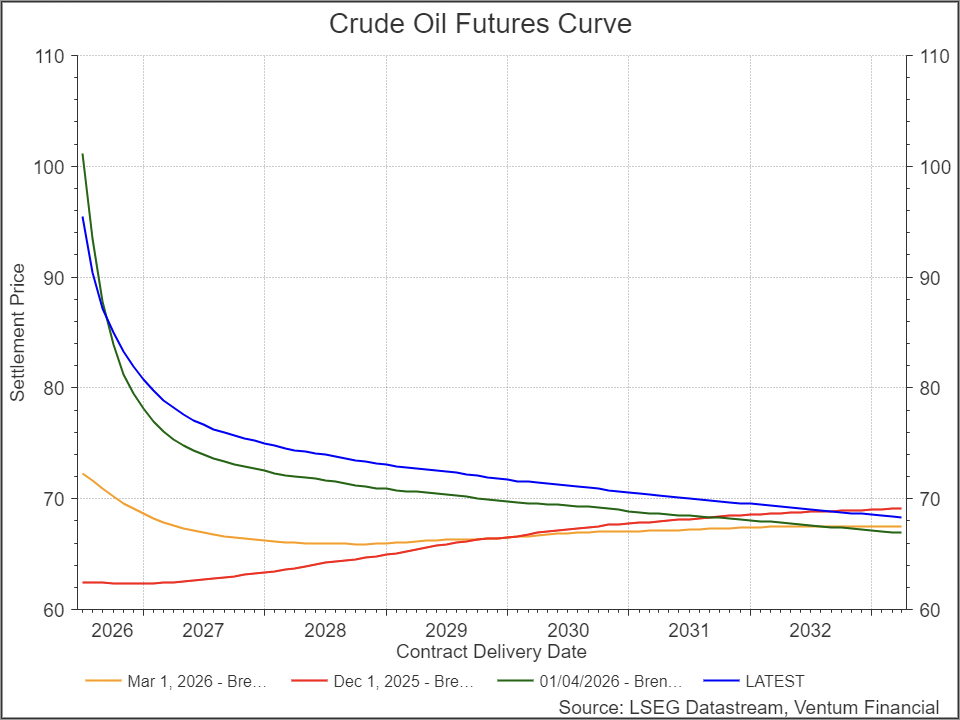

However, the energy picture is more complicated than the spot price suggests. The current U.S.-Iran ceasefire is fragile at best, with both sides — including the IRGC — continuing to make moves that undermine the terms of the agreement. The futures curve reflects this unresolved risk: the April 2027 Brent contract, which traded just above $60/bbl on December 1, 2025, now trades near $75/bbl — a $15 premium that the market is embedding into forward prices well beyond the immediate conflict. Damaged energy infrastructure, lingering supply uncertainty, and the prospect of renewed hostilities are keeping the back end of the curve elevated. Peace may be partially priced in at the front end, but the market is telling us this story is far from over.

Investment Strategy and Outlook

Equity markets have staged a dramatic upturn in April posting record highs for the Nasdaq and the S&P 500. Benchmark indices have been driven by strong performance in the Technology, Communication Services and Consumer Discretionary sectors. In Canada, the Materials (gold), Financials and Technology sectors led gains.

While some easing of the US-Iranian conflict has supported equity prices, it is the broad-based earnings strength, that underpins the higher share prices. Analysts are expecting the strongest 2026 EPS growth for the Canadian Financials, Materials, Tech Hardware and Software Services. In the US, in the past 3 months almost every US technology stock have seen an upward analyst earnings revision. Moreover, every S&P 500 Industry Group is forecast to see revenue and earnings growth in the next 12 months. Although, earnings are highly concentrated with a small number of tech companies e.g. Micron, with is accounting for much of the S&P 500 earnings growth in 2026.

Given this earnings outlook, resilient jobs market and consumer easing Middle East tensions we remain positive on US and Canadian equities. We expect the AI/Semi/Datacenter/Electrification related sectors to be dominant earnings drivers in 2026 along with materials and energy. We prefer the technology, industrials, consumer discretionary, financials, materials sectors. Given our expectations for volatile, but ultimately, lower oil prices in 2026, we are neutral on the energy sector. We are also neutral on the utilities and real estate sectors given our expectations of elevated interest rates in 2026.

We caution investors that the US-Iranian conflict is not over. Markets are pricing in only moderate disruption and near-term normalization. But the conflict is entering a critical point for global energy supplies – especially products like diesel and jet fuel. If the conflict lasts a lot longer, or worsens, we could see much higher prices. Historically, we know that is not good for inflation, the economy and equity prices.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 – 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre – Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.