Canadian and US Economy: The U.S. economy is growing steadily, with early signs of a hiring pickup, even as consumer sentiment hits a record low and the consumer becomes increasingly bifurcated between wealthy boomers and pressured younger or lower income households. Canada’s economy is weaker, with unemployment increasing to 6.9%, though solid real wage growth supports consumption and inflation remains far more muted than in the U.S.

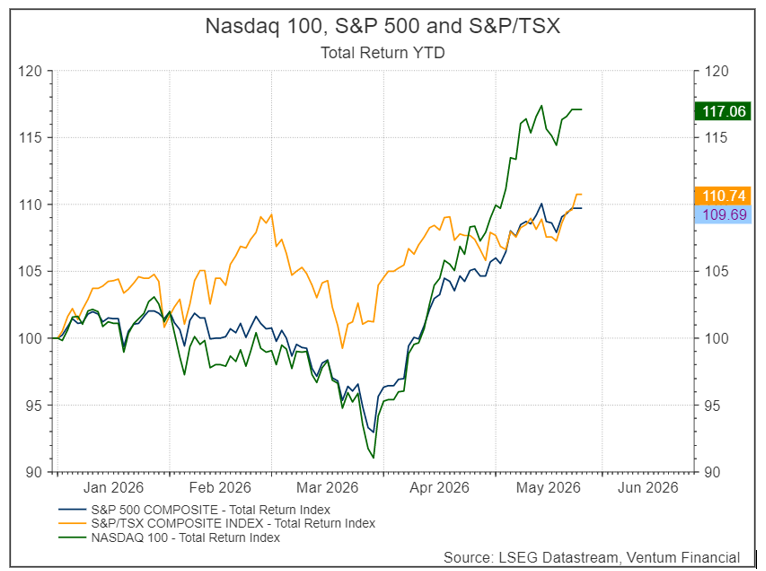

Equity Markets: Equity markets in May pushed to fresh record highs, led once again by technology — semiconductors and hardware in particular — and underpinned by strong, unusually broad-based earnings growth. North American indices posted solid month-to-date gains, with the U.S. outpacing Canada, where heavier energy and gold weightings acted as a drag.

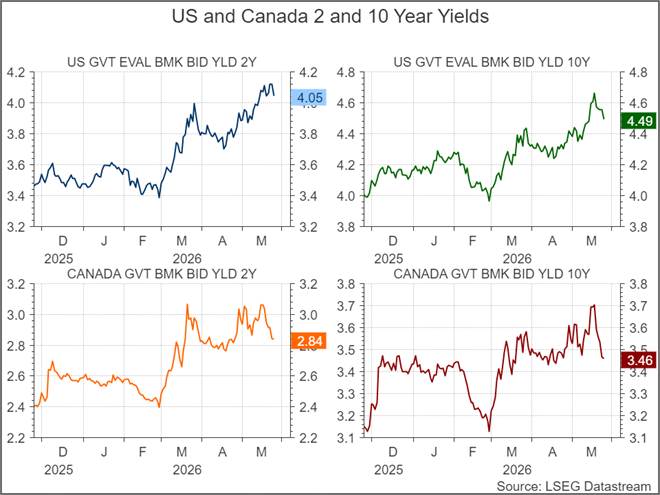

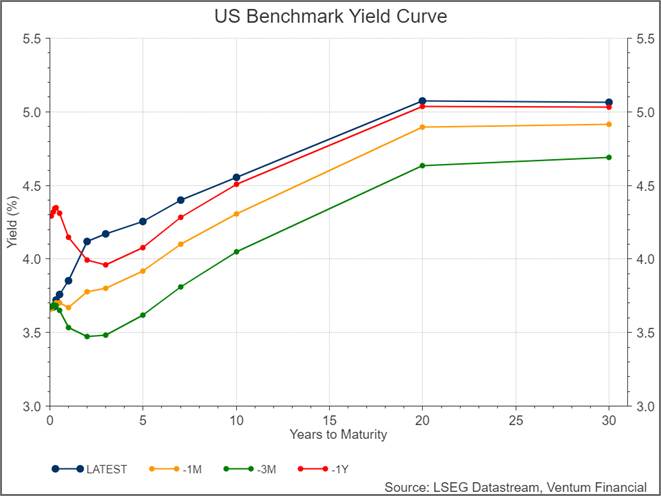

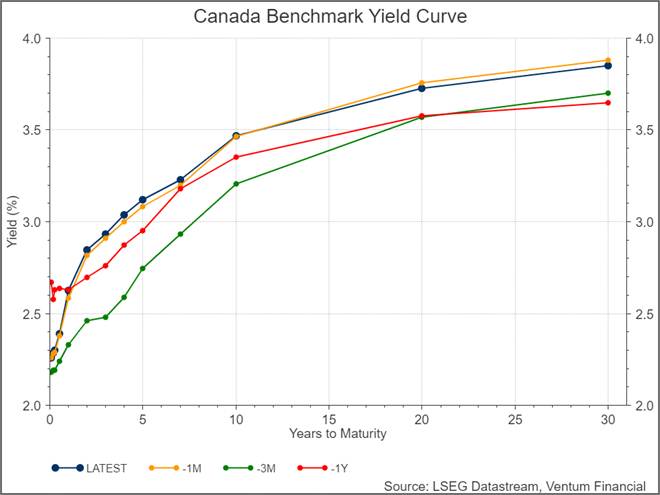

Bond Market: Government yields remain elevated on both sides of the border as inflation reaccelerates on the back of surging energy prices. Bond markets are now pricing in roughly one rate hike over the next 12 months in both the U.S. and Canada. The U.S. curve has shifted higher across the board, while Canada’s reaction has been more contained given its weaker labour market and energy-exporter status.

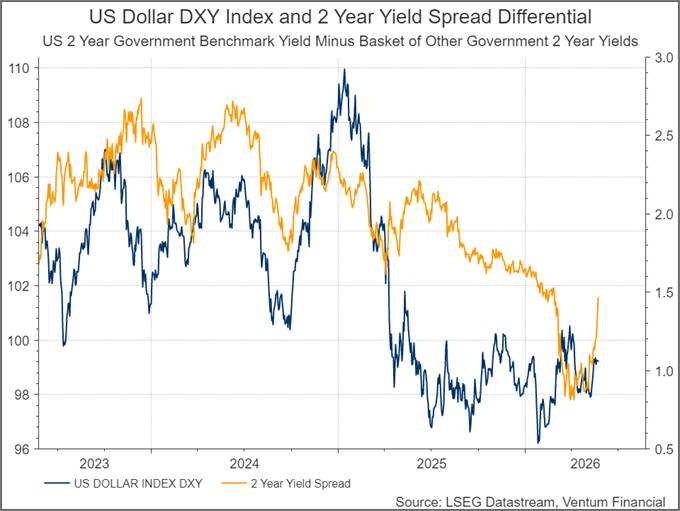

Currencies and commodities: Crude oil has come off its peak but remains elevated, with both WTI and Brent above $90/bbl as the unresolved Middle East conflict keeps pressure on energy markets. We believe strong U.S. growth and its energy-exporter buffer should push the U.S. dollar higher in the near to mid term, with yield spreads pointing to a near-term DXY rebound.

Portfolio Strategy: We remain positive on U.S. and Canadian equities, underpinned by broad-based earnings strength and an AI-led capex cycle spilling into the wider economy, favouring technology, industrials, consumer discretionary, financials and materials. We expect markets to stay volatile and headline-driven, with the main risk being a more persistent energy shock that could force both central banks into rate hikes which we do not think markets are expecting.

Equity Markets

Equity markets pushed to fresh record highs this month, shrugging off the persistent back-and-forth between the U.S. and Iran over peace talks. Despite headlines that swung between ceasefire optimism and renewed tension, investors stayed focused on a strengthening earnings picture — and the broad indices rewarded them for it. The S&P 500 gained 4.95% month to date, while the S&P/TSX Composite added 2.57%, the latter trailing its U.S. counterpart as Canada’s heavier resource weighting continued to act as a drag. Beyond energy, gold prices were a second headwind for the index, declining -3.77% month to date and weighing on the TSX’s sizable materials component.

Crude oil retreated from its recent peak, but the relief has been only partial — both WTI and Brent are still hovering above $90/bbl, a reminder that energy markets remain hostage to the unresolved geopolitical situation. As we have noted, until a durable agreement is reached, oil prices and equity markets will stay volatile and headline driven.

While we are seeing broader participation in the rally, once again, the rally was led by technology. Semiconductors and hardware were the standout performers: the SOXX semiconductor ETF surged 24.35% month to date, while the tech-heavy Nasdaq-100 climbed 9.77%. Software lagged its hardware counterparts but still posted a robust 10.56% gain — a respectable showing in any other month, and a sign of how concentrated leadership has become at the top of the market. The Dow Jones Industrial Average brought up the rear, though its 2.65% gain remains solid and underscores that strength extended well beyond the megacap technology names.

US Economy

The U.S. economy is growing at a solid clip. The Atlanta Fed’s GDPNow model was revised up again this month, with Q2 2026 growth now projected at +4.3% — a marked acceleration from the start-of-year moderation narrative. The strength is broad-based: consumer spending remains the workhorse at +1.95%, tax returns from the IRS this month is helping with a boost. Non-residential investment is holding firm at +0.85% on the back of the AI-driven capex story, and private inventory investment added meaningfully to the upgrade, contributing +1.06% on its own as businesses restock with confidence in forward demand. Inflation, on the other hand, has also seen meaningful increases. Headline CPI is now at 3.8%, significantly higher than the 2.4% at the beginning of the year. Core CPI has been more benign at 2.75%, but still higher than the 2.5% reading in January.

The labour market is showing early signs of a hiring pickup beneath a stable headline. The unemployment rate held at 4.3%, but the non-farm payroll detail tells a more constructive story: the private sector added 123,000 jobs this month, following 190,000 last month — a pace that now runs ahead of last year’s peak, when April 2025 added just 99,000 private-sector jobs. Private hiring appears to be accelerating, even as JOLTS openings remain subdued at 6.8 million, suggesting employers are converting existing demand into actual hires rather than simply posting new openings. The firing side of the ledger looks equally benign: continuing jobless claims have fallen to 1.78 million, a two-and-a-half-year low, indicating that the workers who do lose jobs are being reabsorbed quickly. Taken together — accelerating hiring, contained layoffs — the labour market looks healthier than the “low hire, low fire” characterization of recent quarters.

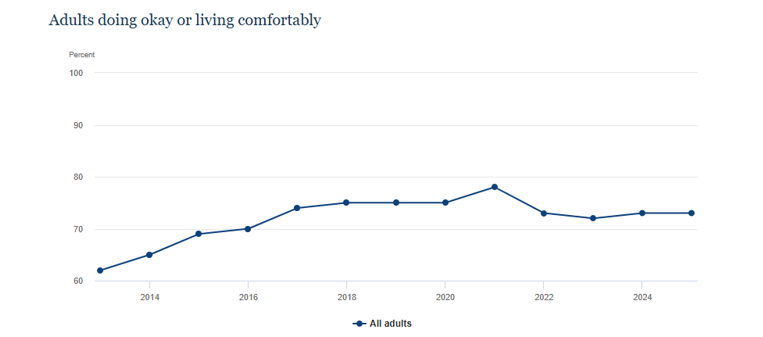

That said, the sentiment data tells a starkly different story. The University of Michigan Consumer Sentiment index fell to a fresh all-time low of 44.8. We read this weakness as driven primarily by anxiety over the war in the Middle East and elevated inflation expectations, rather than by genuine deterioration in household balance sheets. The Fed’s latest SHED survey — released last week, covering 2025 through October — supports that interpretation: the share of households reporting they are doing at least “okay” financially held at 73%, very much in line with prior years.

Beneath that stable headline, however, the divergence between high- and low-income households has widened. Spending by lower-income groups jumped sharply, reflecting their greater exposure to energy and transportation costs — precisely the categories the Middle East conflict has pushed higher.

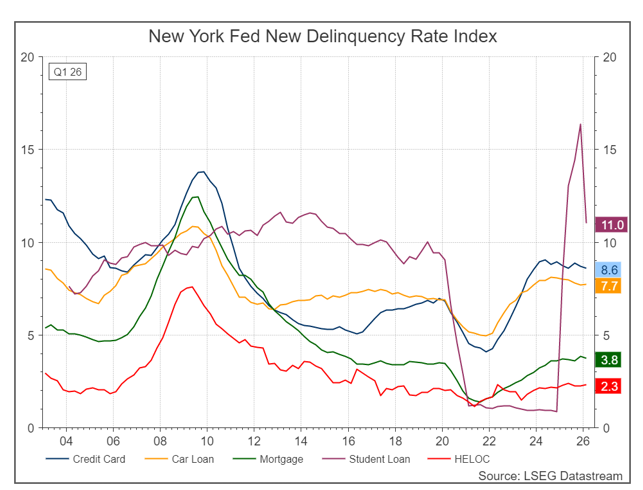

Aggregate delinquency rates remain stable, but the strain is concentrated in younger cohorts, who face the dual squeeze of subdued job openings and a higher cost of living. Student loan delinquency is the clearest symptom: it spiked above 15% in Q4 2025 before easing to 11% in Q1 2026 — still the highest level on record.

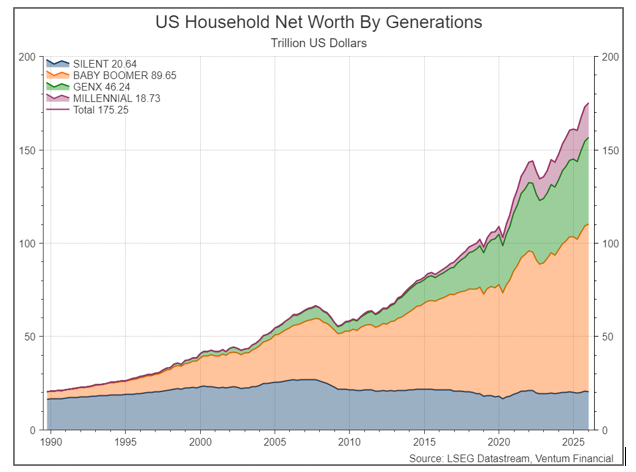

Older households, by contrast, are in far better shape. Total U.S. household wealth sits at an all-time high of $175 trillion, with baby boomers alone accounting for nearly $90 trillion. With that cohort now entering retirement, we would expect their consumption to stay elevated and their savings rate to decline from here — a meaningful, if narrowly based, pillar of support for overall spending.

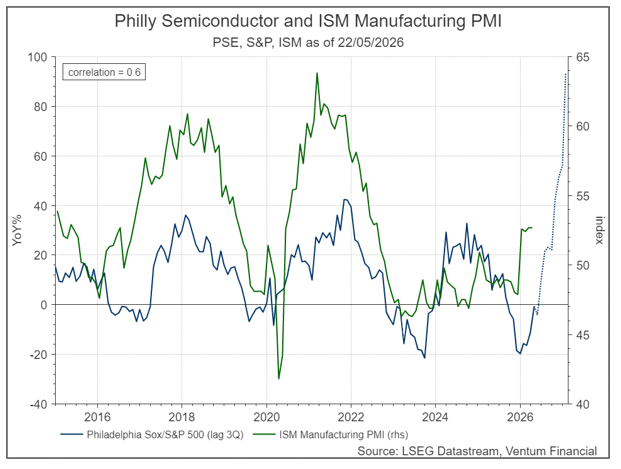

On the corporate front, we see signs that the AI-induced capex boom is beginning to spill over into a broader manufacturing recovery. The Philadelphia Semiconductor Index (SOX), which tracks the 30 largest semiconductor companies, has historically shown a high correlation with — and tends to lead — the ISM Manufacturing PMI. That index is now making fresh all-time highs, with its one-year return approaching a remarkable 100%. If the historical relationship holds, this points to a manufacturing upturn working its way through the broader economy in the months ahead.

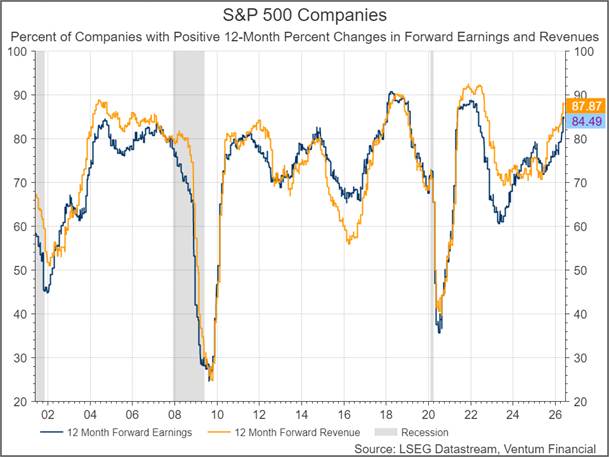

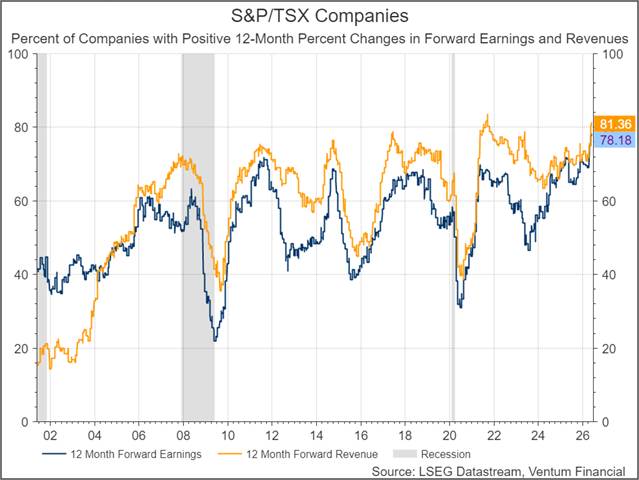

What is especially striking about this cycle is that forward earnings growth is not only strong but unusually broad. The 12-month forward EPS growth estimate for the S&P 500 continues to march higher, now at 19.78%. More notable still is the breadth: the share of companies with positive 12-month forward earnings and revenue revisions has reached 84.5% and 87.9% respectively — among the highest readings in the past 25 years. This is not a rally resting on a handful of megacap names; the earnings strength is widely distributed across the index.

We expect consumption to remain resilient, underpinned by solid jobs market, rising wages, elevated household wealth and an aging population entering its higher-spending retirement years. On the corporate front, the AI-led capex expansion — the main engine of this cycle — is spilling over into adjacent sectors and lifting manufacturing sentiment across the broader economy. With strong earnings behind it, U.S. growth should see a healthy boost. The principal risks remain higher inflation and higher interest rates.

Canadian Economy

By comparison, the Canadian growth picture is considerably weaker. The unemployment rate ticked up again to 6.9% from the prior month, and on a year-to-date basis Canada has shed over 110,000 jobs through the first four months of the year. As we noted in our February report, part of this softness reflects population decline rather than pure demand weakness — Canada’s population contracted -0.2% as temporary workers left the country in late 2025, the largest such exodus in the nation’s history. Wages, on the other hand, continue to grow at a solid pace of 4.8% year-over-year, supported by this structural tightening in labour supply. The consumer is holding up better than the jobs data alone would suggest with March retail sales growing 3.4% year-over-year, and the core measure excluding motor vehicles growing a stronger 5.6%.

The inflation picture in Canada has been considerably more muted. This partly reflects Canada’s status as a major energy exporter, which insulates it from some of the pump-price pass-through hurting U.S. consumers, and partly the housing dynamic — population decline is generating a far stronger disinflationary pull through shelter costs than anything seen in the U.S. Headline CPI reached 2.8% in April, while the core measure actually declined to 2.1%. The Bank of Canada’s preferred trim and median measures, which strip out volatile components, both saw meaningful declines as well. The shelter index — which accounts for roughly 30% of household spending — continues to run below the BoC’s 2% target, and remains a powerful disinflationary force for the Canadian economy. Rental vacancy rates have climbed to or near record highs across many Canadian cities as rents decline, reflecting higher supply and reinforcing the downward pressure on shelter costs.

On the corporate front, the 12-month forward EPS growth estimate for Canadian companies remains elevated at over 20%, and — as in the U.S. — the breadth of that growth is unusually wide. The share of companies with positive 12-month forward earnings and revenue revisions has reached over 78% and 81% respectively, among the widest readings in the past 25 years. Part of this strength reflects elevated energy prices stemming from the war in the Middle East, while another part stems from the broader electrification theme, which has pushed up prices of commodities such as copper. Beyond commodities, the AI-led capex boom in the U.S. and many of Canada’s own federally led infrastructure projects are beginning to seep into earnings expectations.

Canada’s labour market remains weak amid persistent uncertainty, but solid real wage growth and rising net worth due to surging equity markets is supporting consumption even as population growth turns negative. Higher energy prices are lifting the energy sector, while the electrification theme is driving many of Canada’s cyclical companies to fresh all-time highs. We remain bullish on Canada: we believe an investment-led growth cycle will reignite animal spirits among cyclical companies in the mining and automotive sectors. Meanwhile, subdued inflation gives the Bank of Canada room to maneuver should the economy weaken.

Sector Performance – Tech continues to lead

The sector data tells two very different stories on either side of the border.

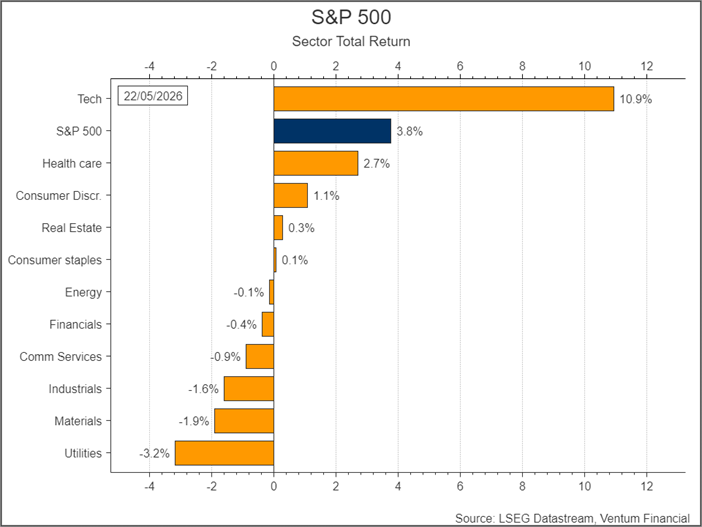

The S&P 500, performance was heavily concentrated: Technology dominated with a +10.9% total return month to date, far outpacing the S&P 500’s +3.8% and leaving every other sector clustered near or below the flatline. Health Care (+2.7%) and Consumer Discretionary (+1.1%) were the only other gainers of note, while Utilities (-3.2%), Materials (-1.9%) and Industrials (-1.6%) lagged. The picture is one of a market carried almost entirely by the AI and semiconductor trade, with breadth notably thin beneath the surface.

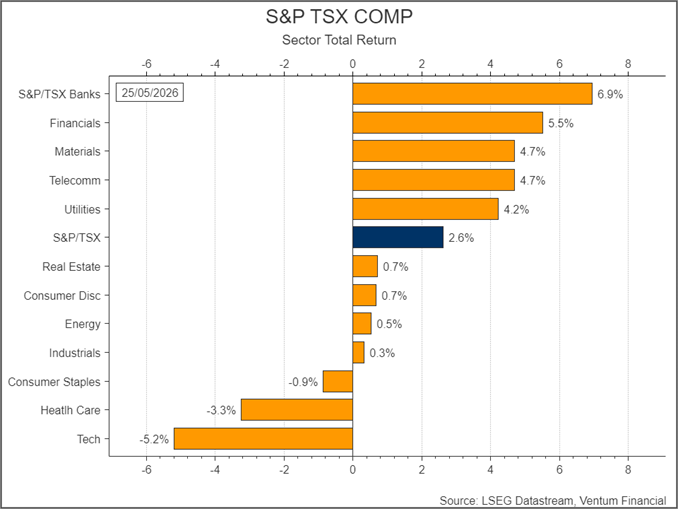

For the S&P/TSX, leadership was both broader and almost the mirror image of the U.S. The S&P/TSX returned +2.6%, but the gains were led by rate-sensitive and resource sectors rather than technology: Banks (+6.9%) and Financials (+5.5%) topped the table, followed by Materials and Telecom (both +4.7%) and Utilities (+4.2%). Tech was the standout laggard at -5.2% — a striking contrast to its U.S. counterpart — with Health Care (-3.3%) also falling. The TSX’s diversified, value-tilted composition meant participation was far wider than in the U.S., even if the headline index gain was more modest.

Bond Market

Government yields remain elevated on both sides of the border, with little sign that markets have grown comfortable that the inflation threat has passed. In the U.S., the 2-year Treasury yield sits at 4.05% and the 10-year at 4.49%, both having pushed higher through the spring and now trading near the top of their ranges since late 2025. Canadian yields tell a similar story, with the 2-year at 2.84% and the 10-year at 3.46% — also well above where they began the year. The persistent climb reflects a market repricing for stickier inflation and a higher-for-longer rate path, driven in large part by the energy shock from the Middle East conflict.

The level of inflation leaves both the Bank of Canada and the U.S. Fed with little room to ease in the near term. With headline inflation reaccelerating and crude still above $90/bbl, markets in both countries are now pricing in rate hikes — each discounting roughly one hike over the next 12 months. The U.S. yield curve has shifted higher across the board, with the 2-year showing the largest rise since the Middle East conflict began in early March, reflecting how sharply expectations have repriced toward tightening.

Canada’s reaction has been more contained, however, held back by its weaker labour market and its position as a major energy exporter, which together blunt the inflation impulse the U.S. is now confronting.

Currencies

On the currency front, we believe the strength of the U.S. growth picture should push the dollar higher in the near to mid term. Unlike the U.S., which is a net energy exporter, Europe and Japan enjoy no such buffer — weaker growth and a faster pass-through of higher energy prices into domestic inflation are dampening their economic prospects. This divergence is increasingly visible in rate markets: the basket-weighted 2-year yield spread between the U.S. and the six DXY constituent currencies has widened in the dollar’s favour, a relationship that has historically led the index and now points to a near-term rebound in the DXY.

Investment Strategy and Outlook

The ultimate drivers for equity prices, corporate revenue and earnings growth, remain positive and keep us optimistic for equity prices. Forward 12-month EPS growth estimates are continuing to march higher in both markets — above 20% in Canada and approaching 20% in the US. Moreover, the breadth of that growth is among the widest in 25 years, and with most companies seeing both positive forward earnings and revenue revisions. We see clear signs that the AI-led capex boom, will be durable and is spilling beyond technology, lifting manufacturing sentiment and adjacent industrial and materials sectors on both sides of the border.

This positive earnings outlook is also being driven by a resilient no fire-no hire US jobs market, a wealthy consumer, rising wages, surging household wealth and an aging high spending baby boomer.

Although return on all this AI capex continues, we think we are still in the early innings and expect the AI / semiconductor / datacenter / electrification complex capex build out to continue into 2027 and to be the dominant earnings driver, alongside materials and energy in 2026.

However, we caution investors that there are several red flags to watch out for; equity markets have done extremely well and thus leave little room for disappointments. Interest rates and inflationary expectations have risen substantially due to much higher energy prices which are pressuring consumption and economic growth.. Valuations are high for many companies and sectors. For example, our Canadian banks are at or near to highest valuation levels on record. In the U.S., the S&P 500 or Nasdaq benchmarks are heavily concentrated, driven almost entirely by the Technology sector and the semiconductor and hardware stocks.

We prefer the technology, industrials, consumer discretionary, financials and materials sectors. Given our expectation for elevated interest rates through 2026, we are neutral on the utilities and real estate sectors. The principal risks to our view remain higher inflation and higher interest rates, particularly should the energy shock from the Middle East prove more persistent than markets currently expect.

We caution investors that the US-Iranian conflict remains unresolved. Markets have largely looked through the geopolitical risk, pricing in only moderate disruption and a near-term normalization of energy supplies. But with both WTI and Brent still above $90/bbl, the conflict continues to keep upward pressure on global energy markets — and on refined products such as diesel and jet fuel in particular. Should the conflict drag on or escalate, prices could move materially higher. History tells us that an energy shock of that kind is not good for inflation, for the economy, or for equity prices — and it is precisely the scenario that would force the Fed and the Bank of Canada from a hold into outright hikes.

Han Li . MA CFA

Bert Quattrociocchi, BA CFA

Discretionary Asset Management and Portfolio Strategy

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 – 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre – Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.