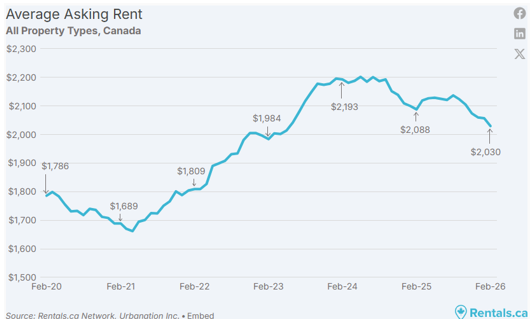

Recent data from Rentals.ca has shed light on evolving conditions in Canada’s rental housing market. The average asking rent across the country declined to $2,030 in the most recent month, returning to levels last seen in 2023.

In the period following COVID-19, Canada experienced an influx of international students and temporary workers that significantly increased housing demand in a short period of time, contributing to a sharp tightening in rental supply. The recent easing in rents appears to reflect a partial reversal of that trend. Federal policy changes—including caps on international student permits and tighter restrictions on temporary workers—combined with the departure of some existing students and workers, have slowed population growth and reduced pressure on the rental market.

While there are areas worthy of optimism—most notably the improvement in rental affordability, with average rent as a percentage of household income falling below 30% for the first time since February 2021—we continue to see several developments that may present potential risks.

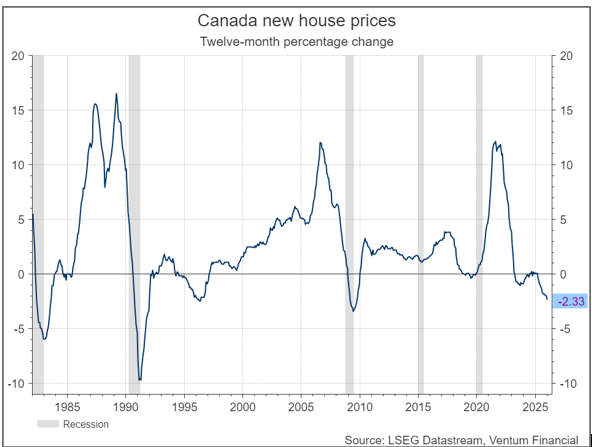

The first risk is the continued decline in property prices, with year-over-year price changes remaining negative since the start of 2025. If housing prices continue to fall, residential developers could face increasing pressure. As prices decline, the spread between construction costs and the eventual sale price narrows, eroding project profitability. This dynamic could lead to a rise in project cancellations or delays, particularly in the condominium markets of Toronto and Vancouver, where meeting pre-sale thresholds has already become more challenging in early 2026.

A second area of risk lies within the banking sector. While Canadian banks are generally conservative in their lending practices, a sustained decline in home prices would likely lead to higher provisions for credit losses (PCL). In such a scenario, the focus shifts from whether borrowers can continue servicing their mortgages to whether the underlying collateral—the home itself—adequately supports the value of the loan. At present, we assign a low probability to this outcome, as banks have already been gradually increasing their PCL buffers. However, a sudden shift in interest rates or broader economic conditions could alter that outlook.

The third risk is the broader macroeconomic impact stemming from the conflict in the Middle East. The closure of the Strait of Hormuz has caused energy prices to surge. At the time of writing, Brent Crude Oil is hovering just above $100 per barrel, levels not seen since the early stages of the Russian invasion of Ukraine.

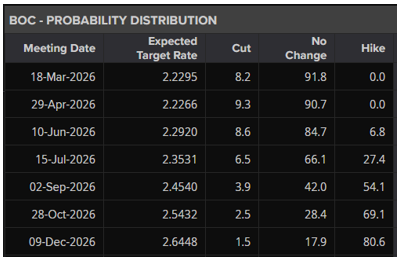

The impact has quickly transmitted into interest rates. Canada’s 2-year government bond yield has risen from roughly 2.4% on February 27 to over 2.8% by March 12, an increase of more than 40 basis points in just two weeks. As a result, markets are now assigning roughly a 50% probability that the Bank of Canada could raise interest rates as early as September.

For now, market expectations remain anchored to the assumption that the conflict will be relatively short-lived, with some estimates—including comments from Donald Trump—suggesting the war could end within six weeks. However, we caution that the longer the conflict persists, the greater the strain on financial markets. Sustained energy price increases risk pushing interest rates higher, which in turn places downward pressure on the valuation of most asset classes.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 – 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre – Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.