The start to the new year has been anything but smooth for markets. Geopolitical concerns have rattled investor sentiment and injected fresh uncertainty into global asset prices. Year-to-date, the Dow is up 2.15% to Friday’s close, outperforming the Nasdaq 100 (+1.41%) and the S&P 500 (+1.02%). Headlines surrounding a dramatic U.S. military operation in Venezuela — including the capture of President Maduro and moves to assert control over the country’s oil sector — have kept risk premiums elevated and forced investors to reassess geopolitical risk.

Meanwhile, President Trump’s provocative comments regarding Greenland, including talk of buying or expanding U.S. influence over the strategically important territory and escalating diplomatic tensions with European allies, have added to market volatility. At the same time, renewed tensions with Iran — marked by heightened military posturing and the risk of further escalation — have compounded an already fragile geopolitical backdrop.

Yet despite the sabre-rattling and headline risk, the U.S. economy has shown surprising resilience. According to the Atlanta Fed’s GDPNow model, real GDP growth in the fourth quarter of 2025 is being tracked at roughly 5.4% annualized, one of the strongest quarterly growth rates in recent memory. The key drivers of this group include the massive AI/datacenter capex spending, a supportive jobs market, rising net worth thanks to surging equity prices and stimulative US government fiscal and monetary policies. Consumer spending alone is expected to contribute approximately 2.15 percentage points to quarterly GDP growth, underscoring the continued strength of household demand despite softer consumer sentiment readings.

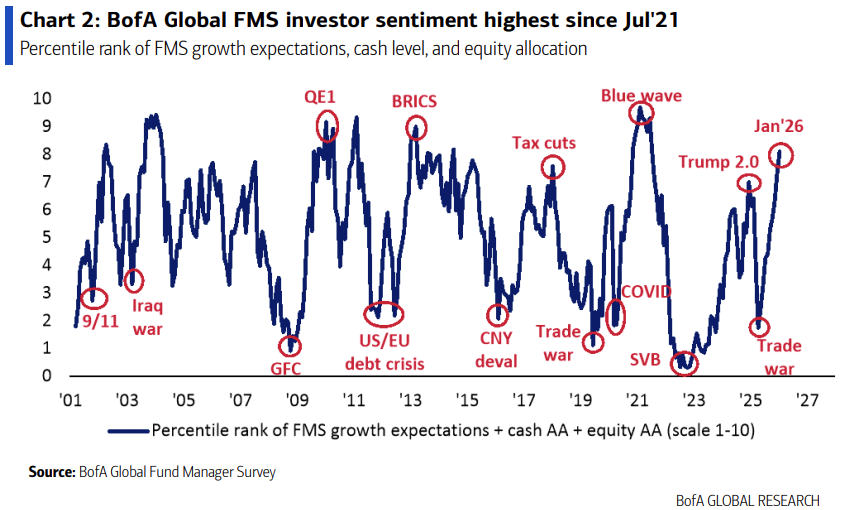

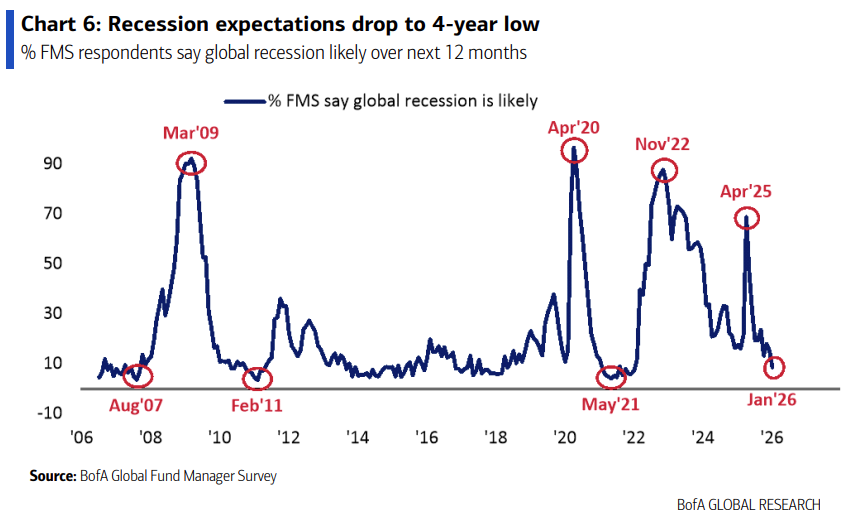

That underlying economic momentum is increasingly reflected in investor positioning. BofA Global Fund Manager Survey data shows sentiment has climbed to its highest level since mid-2021, while the share of managers expecting a recession over the next 12 months has fallen to a four-year low. Together, these shifts suggest markets have, for now, chosen to focus on economic fundamentals, with optimism more than offsetting ongoing geopolitical uncertainty.

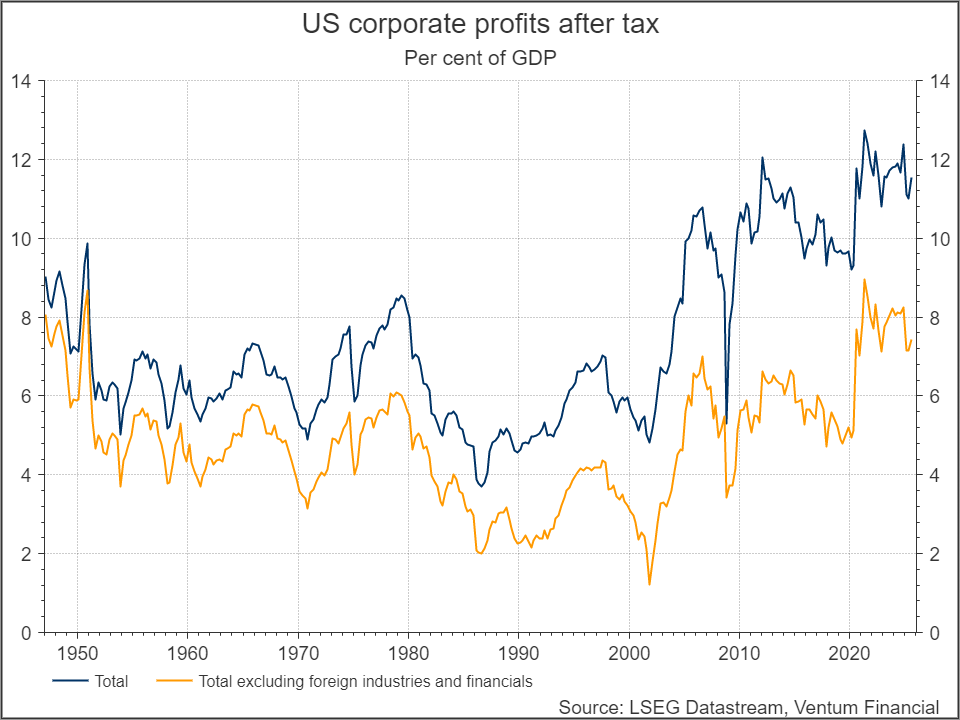

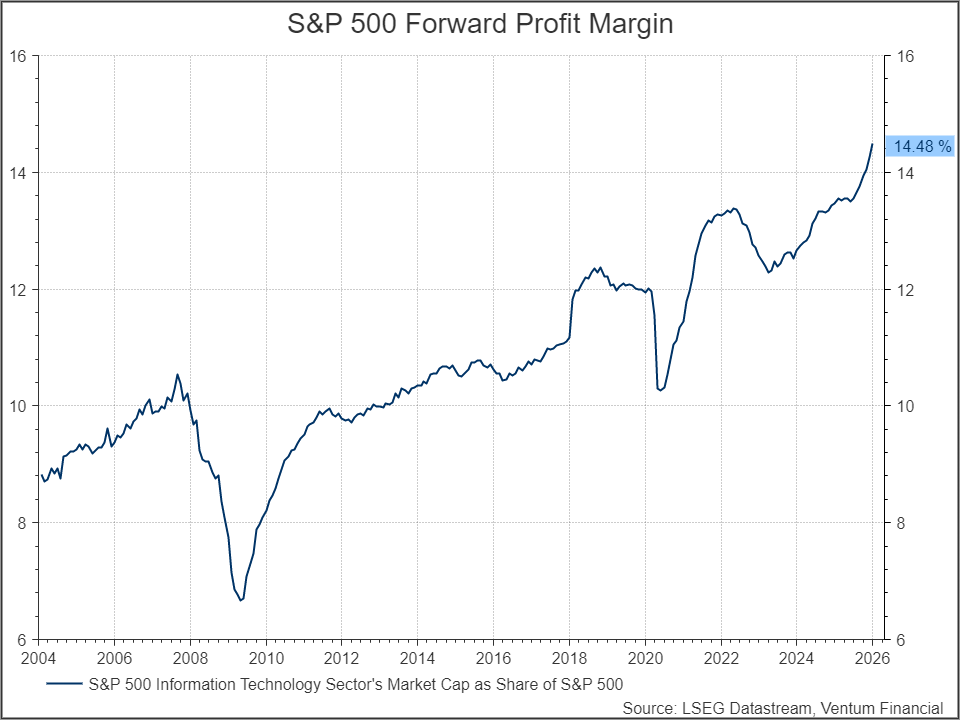

The resilience of the economic expansion is mirrored in the corporate sector. U.S. after-tax corporate profits as a share of GDP are currently among the highest in history, supported by the ongoing AI revolution and recent fiscal legislation that is expected to extend corporate tax cuts into 2028—underpinning earnings expectations and equity valuations.

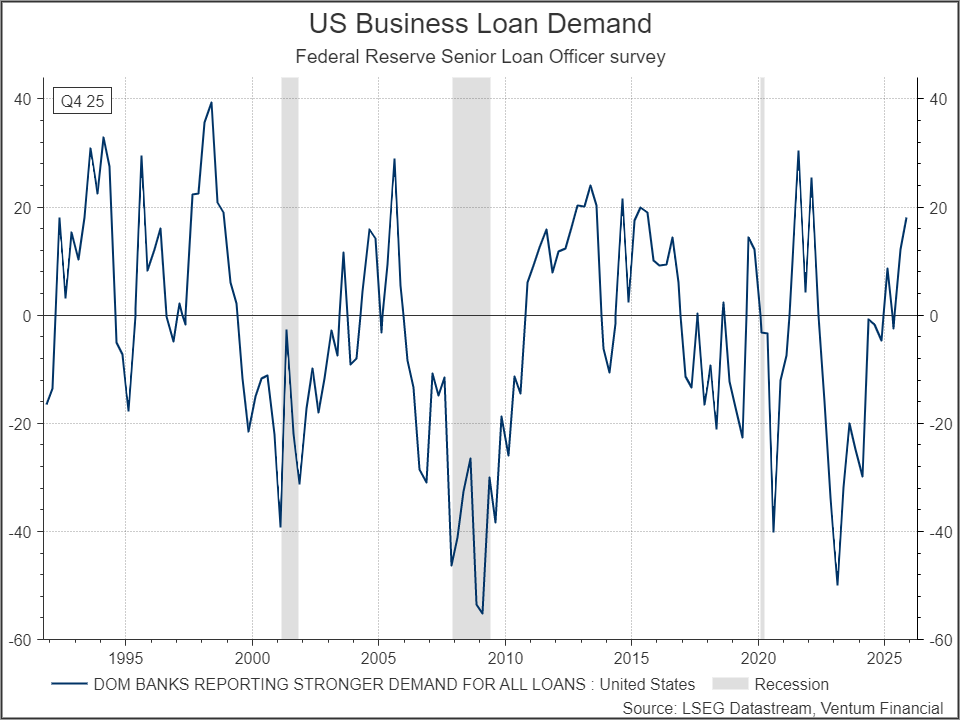

Business loan demand, which fell sharply in 2023, has turned a corner and pushed back toward expansionary territory, with the index rising to levels not seen since 2021, suggesting credit conditions for firms are easing.

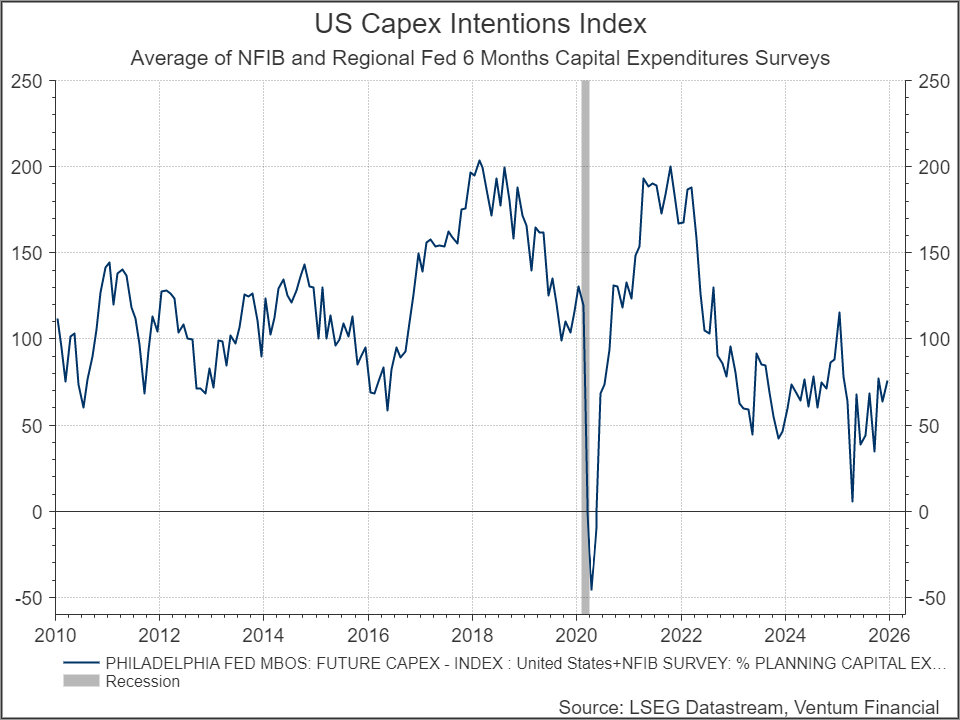

Moreover, surveys of capital expenditure intentions — including NFIB and regional Federal Reserve measures — have been trending higher since last year’s lows, pointing to firms planning increased capex over the coming months, a positive signal for productivity gains and future growth.

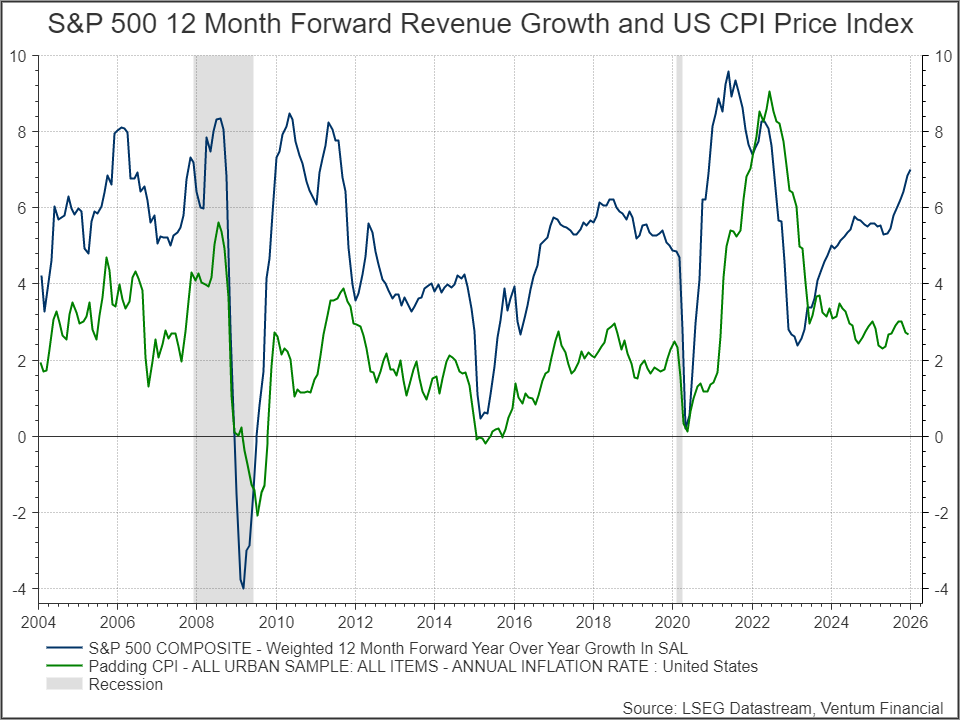

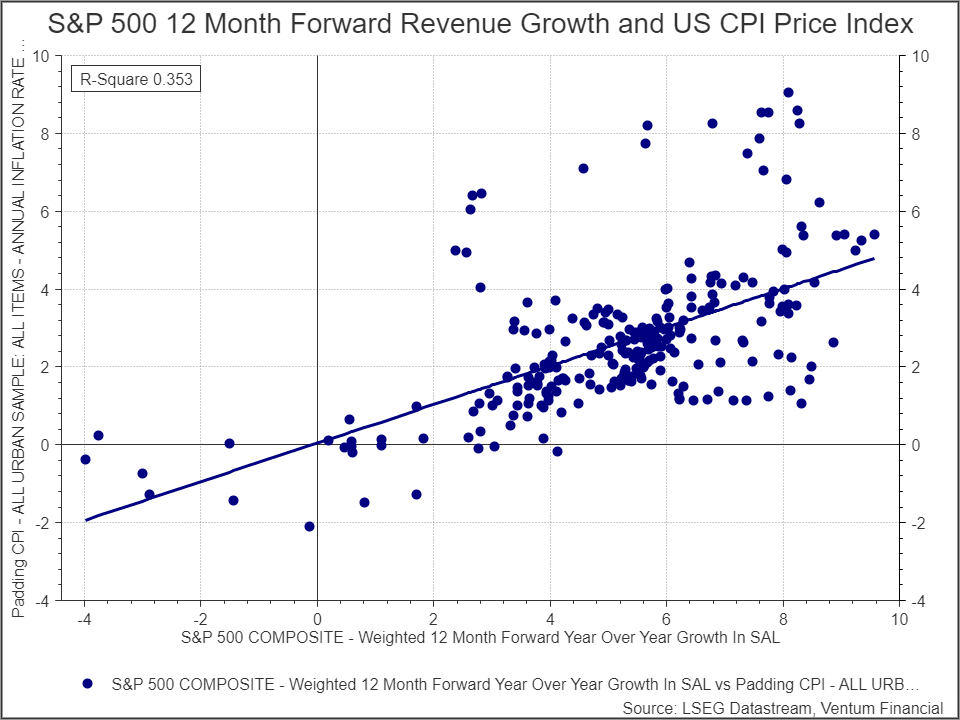

Forward-looking earnings and revenue indicators also remain elevated, though it’s important to note the relationship between growth and inflation expectations: as forward revenue growth increases, markets often price in higher inflation (and by extension, higher interest rates), a dynamic visible in the historical correlation between the S&P 500’s forward revenue growth and U.S. CPI.

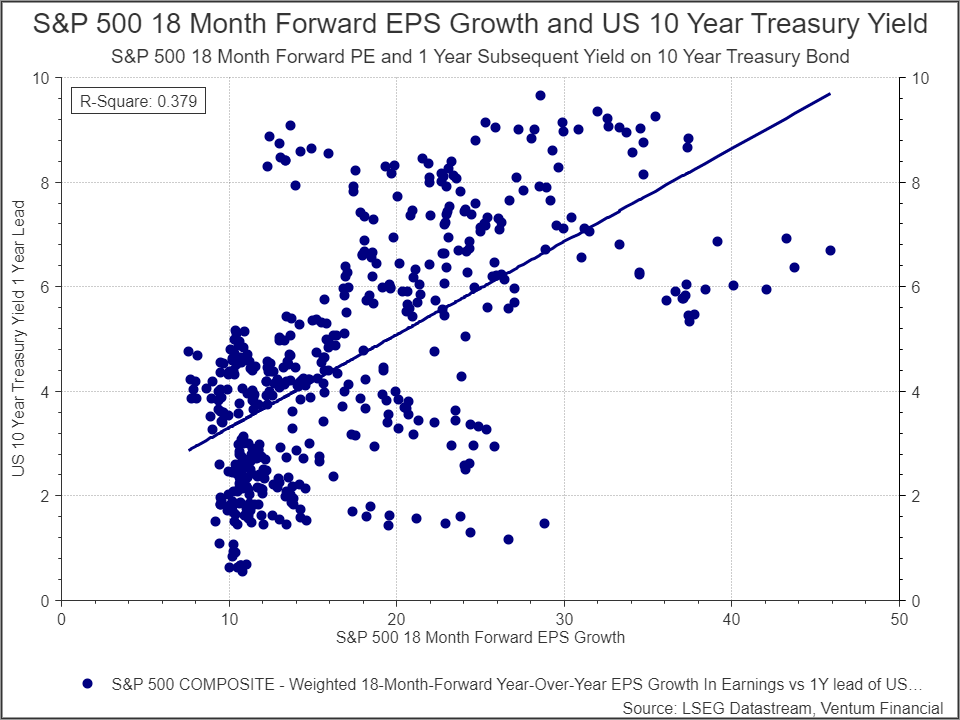

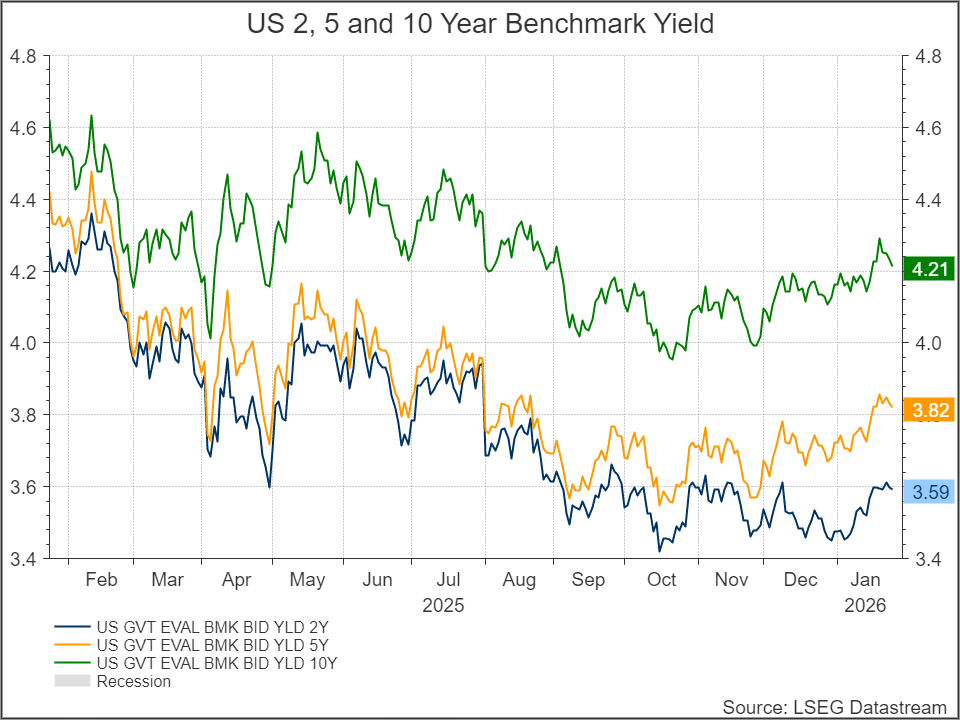

This backdrop of vibrant growth — if sustained — carries meaningful implications for financial conditions. Higher expected earnings, as reflected in forward EPS growth, have historically coincided with higher 10-year Treasury yields in the year that follows, underscoring the risk that continued economic strength could re-ignite rate-normalization pressures, particularly in an environment where inflation expectations remain above pre-pandemic norms. Reflecting these dynamics, the U.S. 10-year Treasury yield briefly rose above 4.25% this week following President Trump’s remarks on Iran and Greenland, before settling at 4.23% as of Friday’s close.

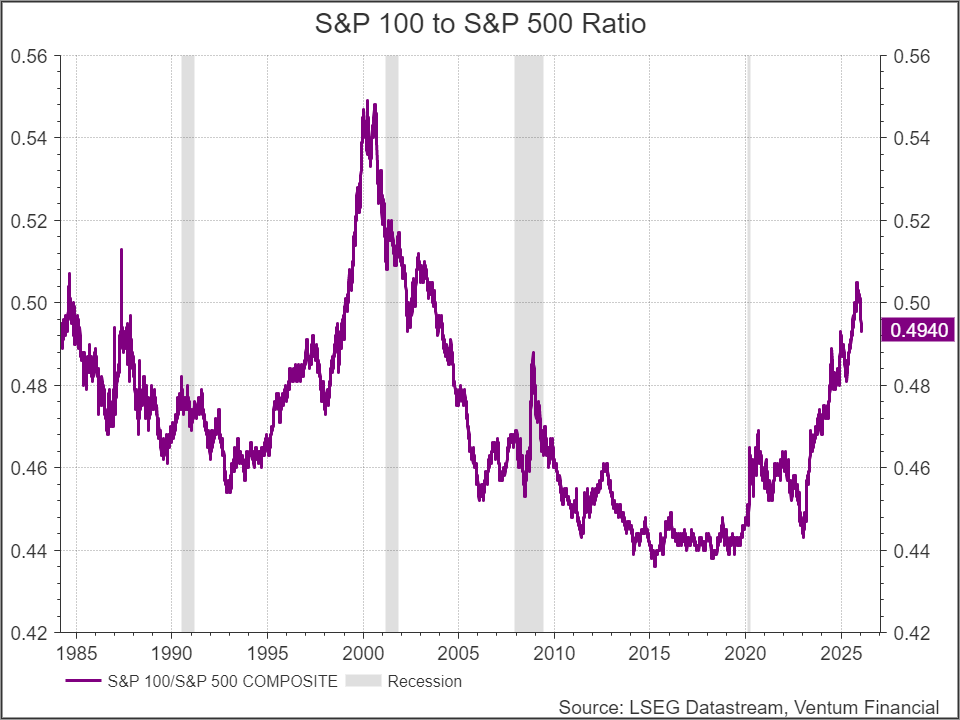

From a market-structure perspective, there are early signs that investors are beginning to rotate away from the largest U.S. stocks. Mega-cap companies delivered exceptional performance through much of 2025, but their strong gains have increasingly drawn attention to valuation. Historically, periods of extreme concentration have tended to coincide with inflection points in leadership. During the technology bubble of 2000, the S&P 100–to–S&P 500 ratio peaked near 0.55 before entering a prolonged decline. In the current cycle, the ratio topped just above 0.50 in November and has since begun to roll over — a development that suggests capital is gradually rotating out of the largest names and into smaller constituents within the broader index.

A similar dynamic is emerging beneath the surface in style leadership. After an extended period of growth outperformance, value has begun to regain ground, with value indices overtaking growth over the past three months. While still early, the combination of easing mega-cap concentration and a nascent value rotation points to a market that is broadening — a characteristic more commonly associated with mid-cycle expansions than late-cycle excess.

Rising bond yields remain the clearest fault line in this otherwise constructive narrative. While resilient growth and improving earnings support risk assets, higher yields challenge the valuation framework that underpinned mega-cap dominance. If rate pressures persist, markets may continue to reward balance-sheet strength, cash-flow durability, and valuation discipline—further reinforcing the shift away from concentration and toward a broader, more cyclical market leadership.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 – 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre – Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.